|

|

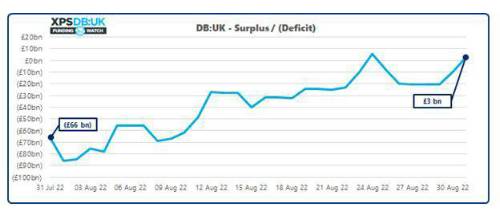

UK pension schemes have become 100% funded on a long-term target basis for the first time since aggregated records began. UK pension scheme deficits against long-term funding targets fell by a further £69bn over the month to 31 August 2022. Gilt yields rose by 0.7% over the period, reducing the value of schemes’ liabilities and continuing the trend seen during 2022. For schemes that are now 100% funded, there may be opportunities to lock in recent gains and to review their ultimate end-game strategy. |

Deficits of UK pension schemes have decreased by c.£69bn over the month to 31 August 2022 against long-term funding targets, an analysis from XPS’s funding tracker XPS DB:UK has revealed. Based on assets of £1,623bn and liabilities of £1,620bn, the aggregate funding level of UK pension schemes on a long-term target basis was 100.2% as of 31 August 2022.

Drivers of the change

Rising gilt yields continued to be the main contributor to improvements in funding levels during August, partially offset by a small rise in long term expectations of inflation. This adds to the improvements in long-term positions that we have seen over 2022 –now in excess of £330bn for the year. Equity markets struggled over August but performance was pushed back into positive territory for many UK pension schemes, due to depreciation of Sterling over the month. Matching assets continued to fall alongside liability values, but this remains beneficial for schemes that are not fully hedged, particularly when looking at longer-term assumptions.

Tom Birkin, Actuary at XPS Pensions Group said: “The DWP launched its long-awaited consultation on DB funding rules and long-term funding objectives at the end of July. However, with the average UK pension scheme now fully funded on a long-term basis, there may not be as many schemes having to take drastic action as a result of the new regulations as once thought. Now is an excellent opportunity for schemes to consider their investment strategies to ‘lock in’ these significant gains and to think about what the ultimate end-game for the scheme might be. This is good news for pension scheme members as securing members benefits is within reach for more schemes than ever before.” |

|

|

|

| Take the lead client-facing projects ... | ||

| Various locations - Negotiable | ||

| Choose Life! Choose a major global co... | ||

| Various locations - Negotiable | ||

| Actuarial skillset? Apply now for Snr... | ||

| South East / hybrid with travel requirements - Negotiable | ||

| Financial Risk Leader - ALM Oversight | ||

| Flex / hybrid - Negotiable | ||

| Be the very model of a modern Capital... | ||

| London - Negotiable | ||

| Pensions Actuary seeking a high-impac... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Great opportunity for Pensions Actuar... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Responsible Investing Manager - Clima... | ||

| London/Hybrid - Negotiable | ||

| Quant Strategist | ||

| London/Hybrid - Negotiable | ||

| Multiple remote longevity contracts | ||

| Fully remote - Negotiable | ||

| Multiple remote inflation hedging con... | ||

| Fully remote - Negotiable | ||

| Play a vital role in shaping a new He... | ||

| London or Scotland / hybrid 50/50 - Negotiable | ||

| Support the Longevity team of a globa... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Delve into financial risk within a ma... | ||

| Wales / South West / hybrid 1dpw office-based - Negotiable | ||

| Project-based Life Pricing Actuarial ... | ||

| South West / hybrid 2 dpw office-based - Negotiable | ||

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

| Develop your career in motor pricing | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Experience real career growth in home... | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Be at the cutting edge of technical p... | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Use your passion for innovation and t... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd