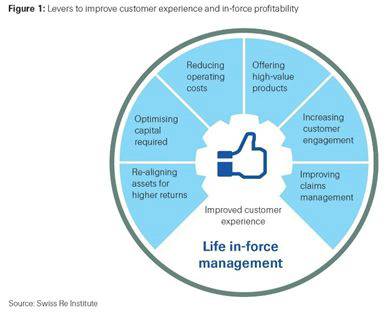

Some insurers are working to cultivate stronger relationships with existing policyholders by steering consumers toward products that better serve their needs, and also by improving the claims management processes. At the same time, insurers are becoming more effective in managing existing portfolios, for instance by using data analytics to improve customer retention rates and reduce operating costs, thereby improving their own profitability. Such actions also ultimately help facilitate lower premiums for consumers.

Traditionally, life insurers have focused on growing new business, but many are currently paying increased attention to enhancing the value of existing portfolios. To do so, they are applying different levers for a more effective management of in-force books (ie, existing business) with the aim of increasing customer satisfaction. For example, insurers use new technologies to detect issues and trends early on. "New technologies such as wearables can be used to strengthen customer engagement and incentivise policyholders to help monitor and ultimately manage their own health status," says Kurt Karl, Swiss Re Chief Economist.

Guiding customers to higher value-added services

Health case management programmes can teach claimants how to best self-manage their health and coordinate their treatment and home nursing to avoid expensive hospital stays. "With these programmes, insurers can offer policyholders with and without existing health issues tailored services that assist them to live healthier and longer lives," Karl continues. Disease management programmes can help policyholders to get back to work sooner after having suffered an illness or condition. This benefits patients, employers and insurers alike:

• Work instils a sense of purpose and provides income to the claimant.

• Employers are able to improve worker productivity, reduce their management costs and lower the costs of temporary staff.

• Insurers can reduce payments on daily allowances and permanent disability pensions.

Consumer satisfaction is an important differentiator for insurers in competitive markets. For example, insurers can enhance customer experience by improving their claims management processes. An insurer known to have an efficient, consumer-friendly claims department is best-placed to retain and win new business.1 This is especially true in health insurance, where claims tend to be made more frequently. The claims process starts when a policy is first sold. Insurers should therefore explain to customers, in simple language, what their policy covers and what it does not. They should also provide customers with clear guidance on how to file a claim, and offer easy access to claims managers when a claim is made, the sigma says.

It's about profitability too

In addition to providing more benefit to consumers, the increased focus on managing their in-force business can help insurers sustain long-term profitability. Retaining customers is an important component in this regard, not least because keeping existing policyholders is less expensive than winning new business. Data analytics can be used to improve customer retention rates in several ways. Statistical models can be applied to investigate which clients may lapse their policies and why, using data systematically collected from different sources beyond traditional policyholder information. Based on the findings, predictive models can then provide forecasts of consumer propensity to lapse in response to changes in different variables, such as additional services. The resulting insights can inform insurers' resource allocation decisions with respect to client retention initiatives.

A main concern for insurers currently is the long-running low interest rate environment. Investment income is a very important earnings stream, particularly for life insurers, and with interest rates expected to remain low, overall profitability in the life sector will likely remain under pressure. As a result, as part of a broader in-force management strategy for improved profitability, some life insurers have realigned their asset allocation to invest a modest amount more in higher-yielding assets.

Capital optimisation is also integral to improving the profitability of in-force business. Reinsurance and capital market solutions provide effective tools to manage capital. One way to provide capital relief is to reduce mortality, morbidity and longevity risk exposures by transferring risks to reinsurers or capital markets. Reinsurance and capital market solutions can also be used to free up trapped capital through solutions which allow insurers to reduce their capital reserves or bring forward the value of future profits.

A final lever to improve profitability of in-force books is to reduce operational costs. Operational inefficiencies are often driven by legacy IT systems, overly-complex business plans and inefficient operating models. All such actions can help reduce the cost of providing insurance, and that ultimately benefits consumers via lower premiums.

The levers described in this sigma on administrating in-force business are not exhaustive. However, those reviewed are all interconnected as part of an effective in-force management strategy. A holistic approach which simultaneously orchestrates multiple activities across the whole of an organisation is needed to be able to deliver sustainable value for consumers and ultimately grow long-term profitability.

|