|

|

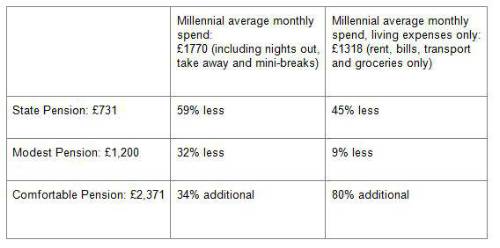

If you’re just kick-starting your career, it can be hard to imagine yourself as a retiree relying on a pension pot. Taking into account everyday expenses, saving for your retirement while you’re still young can seem like less of a necessity, and more of an inconvenience - especially when you could be spending your hard earned money on a night out or a well-deserved holiday. But does this mentality mean that Millennials aren’t actually aware of the consequences they could face in the future without a sustainable pension pot? |

Profile Pensions have analysed the monthly spending habits of Millennials, from necessary living expenses, to flat whites and takeaways, to help illustrate to Millennials their financial state if they don’t at least start thinking about retirement now. How Much Less Will it Really be?

Top Saving Tips

• Take Advantage of Pension Schemes - All workplaces should offer a pension scheme, committing to this means that a portion of your salary (commonly 5%) is dedicated towards retirement for you. Michelle Gribbin, Chief Investment Officer at Profile Pensions commented, “Although monthly expenses can vary from generation to generation, we wanted to showcase to those still climbing the career ladder the necessity of preparing for their financial future early, by highlighting just how much of their current lifestyles they would have to change in order to live comfortably in retirement. Although it can be easy to glance over small indulgences from time to time, it does all add up, and preparing for retirement is key for us all, no matter our age. In fact, as our results show, the earlier you can start saving, the more comfortable your retirement can be. ”

Uncover more about how a Millennial lifestyle translates to a pensioner’s budget, and tips on how to ensure you’re prepared. |

|

|

|

| Take the lead client-facing projects ... | ||

| Various locations - Negotiable | ||

| Choose Life! Choose a major global co... | ||

| Various locations - Negotiable | ||

| Actuarial skillset? Apply now for Snr... | ||

| South East / hybrid with travel requirements - Negotiable | ||

| Financial Risk Leader - ALM Oversight | ||

| Flex / hybrid - Negotiable | ||

| Be the very model of a modern Capital... | ||

| London - Negotiable | ||

| Pensions Actuary seeking a high-impac... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Great opportunity for Pensions Actuar... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Responsible Investing Manager - Clima... | ||

| London/Hybrid - Negotiable | ||

| Quant Strategist | ||

| London/Hybrid - Negotiable | ||

| Multiple remote longevity contracts | ||

| Fully remote - Negotiable | ||

| Multiple remote inflation hedging con... | ||

| Fully remote - Negotiable | ||

| Play a vital role in shaping a new He... | ||

| London or Scotland / hybrid 50/50 - Negotiable | ||

| Support the Longevity team of a globa... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Delve into financial risk within a ma... | ||

| Wales / South West / hybrid 1dpw office-based - Negotiable | ||

| Project-based Life Pricing Actuarial ... | ||

| South West / hybrid 2 dpw office-based - Negotiable | ||

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

| Develop your career in motor pricing | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Experience real career growth in home... | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Be at the cutting edge of technical p... | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Use your passion for innovation and t... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd