|

|

Mooted changes to bring the RPI and CPI closer together could have a significant impact on DB pension

schemes schemes

By Michael Green, Senior Actuarial Assistant, Xafinity

The ONS have launched a consultation on the way the Retail Prices Index is calculated, with a view to bringing it closer to the Consumer Prices Index. Although the options being considered might alter the rate of inflation by a seemingly small amount, the impact on pension schemes could be very significant. In this article we set out the background to the consultation, consider the options being offered and assess the effects each might have.

The background There are other differences between the RPI and CPI that can have a greater effecton the inflation figures from month to month, most notably the inclusion in the RPI of certain housing costs that are excluded from the CPI. However, the systematic nature of the formula effect means that over the long-term it is the single most important difference between the two indices. Indeed, over the last 10 years, annual CPI inflation has come in 0.7% lower than RPI inflation on average, with 0.6% of this being down to the formula effect. Differences in RPI and CPI inflation- 10 year average to May 2012 CPI inflation - 2.55% 'Formula effect - 0.60% Differences in the goods and services in the basket - 0.40% Other differences including the weights given to goods and services - (0.30%) RPI Inflation - 3.25% Over the last year or two there has been a noticeable increase in the formula effect, from a previously steady level of around 0.5% to around 0.9%. This, and the government’s decision in 2010 to link pension and benefit increases to the CPI rather than the RPI, has prompted the ONS to look closely at the formula effect and whether or not it is justifiable.

The options Having considered the expert advice the ONSset out its consultation, which offers four options for the future calculation of the RPI. They are:

1 – Leave the RPI calculation as it is. The formula effect would remain close to its current level of 0.9%

2 – Amend the RPI calculation to bring it into line with the CPI for limited categories of goods, such as clothing. This has been estimated to reduce RPI inflation by around 0.5% each year, bringing the formula effect down to around 0.4%.

3 –Bring the RPI calculation into line with the CPI for all categories of goods in which the RPI uses the Carli method. This would reduce RPI by a little under 0.9% each year bringing the formula effect close to zero.

4 – Bring the RPI formula into line with the CPI formula for all categories of goods. This would eliminate the formula effect entirely, leaving only the differences in the baskets of goods. RPI would be reduced by around 0.9% each year.

If option 3 or option 4 were implemented there would be a significant impact on pension scheme liabilities and the prices of RPI-linked assets.

Will changes come to pass, and if so when?

Any move to alter the way the statistics are calculatedfundamentally could ultimately fall foul of legislation designed to protect the interests of holders of RPI-linked bonds –and that might well mean the Chancellor having to sign off any changes.Certainly, a reduced level of RPI would be beneficial to some aspects of the government’s finances over the medium to long term, but therecould well be an outcry from those who would stand to lose from the change, including many overseas investors. This would amount to a significant loss of confidence in UK gilts, makingit politically difficult to justify.As to timing, it is currently suggested that any change could be implemented from March 2013. Given the likely need for referral to the Bank of England and the Chancellor before making a change this seems quite a demanding timescale and some delay is very possible.

Inclusion of housing costs in a new CPI index

From next year there will be a new variant of the CPI index that includes more elements of housing costs. The new index is likely to be known as CPIH and could potentially be adopted by the government for pension increases in place of the CPI. However the method that appears to have been chosen to incorporate owner-occupied housing costs is likely to mean that CPIH does not differ much from the existing CPI over the long–term – perhaps by as little as 10 basis points.

The effect on the markets

Index-linked government bonds pay interest based on the level of RPI inflation. If there were to be a fundamental change that reduced future RPI, investors in index-linked bonds would stand to receive smaller future interest payments. Some would sell their investments and the price of index-linked bonds would fall. Thus, if the formula effect were eliminated, the holders of RPI-linked gilts (and RPI-linked swaps) would see material losses in the short term and perhaps a lesser future return. The extent to which the prices of RPI-linked assets would fall is hard to predict. A significant proportion of index-linked bonds isheld by pension schemes and insurance companies to hedge against long-term inflation risks and such institutional investors might not be as sensitive to changes in anticipated future inflation as private investors. In addition, it is not clear to what extent any changes have already been priced into gilt markets. While the total returns on conventional and index-linked stocks have drifted apart since mid-2012, the divergence has been gradual and it is difficult to attribute it directly to any particular cause.

The effect on pension schemes

Where a pension scheme has some benefits linked to the RPI, a change that reduces RPI inflation would reduce the benefits ultimately received by members, lessening the cost of the scheme to the sponsor. For a scheme with all benefits linked to the RPI, the reduction in overall costs could be as much as 15%. On the other hand, where a scheme matches those liabilities by holding RPI-linked bonds, these would either fall in valuein the short term or give a lesser return over the long term.

Whether the overall effect is beneficial, neutral or detrimental for any given scheme will depend on the extent to which that scheme’s assets match its liabilities and whether the liabilities are linked predominantly to the RPI or the CPI. The regular funding valuations of schemes are based on assumptions derived from financial market statistics. As a result, any savings in the liabilities resulting from changes in the RPI would only be felt in valuation results to the extent that markets react to those changes. When it comes to CPI-linked benefits, there are no matching investments from which to derive actuarial assumptions. Instead, the value placed on CPI-linked benefits depends on market-implied RPI inflation and the trustees’ or actuary’s view of the RPI/CPI gap. If RPI inflation is reduced the assumed RPI/CPI gap will narrow, leaving the anticipated level of CPI inflation broadly unchanged.

Investment strategy decisions

The decision to purchase or retain RPI-linked assets always requires careful consideration, but this is heightened by the uncertainty around the future calculation of the RPI and the impact it might have on asset prices. The key considerations are:

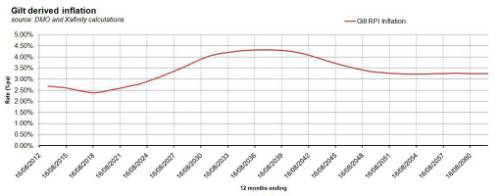

• The characteristics of the scheme’s liabilities and the extent to which they are linked to RPI and/or CPI inflation • The current pricing of inflation – the rates of RPI inflation that can currently be locked into over the period up to 2025 are relatively close to the Bank of England’s target rate and might not appear unattractive, even with a revision to the RPI formula. The chart below shows the year-on-year inflation rates implied by gilt prices at a recent date.

Trustees who currently hold RPI-linked assets may be tempted to reduce their exposure in order to avoid falls in asset prices if the formula effect is completely removed, ie to reduce the extent of hedging. On the other hand, if the RPI is not modified, higher rates of RPI may start to be priced into markets and schemes with smaller holdings of index-linked assets would be exposed to rises in liabilities without the benefit of a matching asset. This is not an easy balance to strike. As ever, investment strategy decisions require very careful consideration and scheme-specificinvestment advice.

What is the problem with the RPI?

The difference between the mathematical approaches used to calculate the RPI and CPI lies in the way that price increases are averaged for similar goods which consumers could easily switch between. The RPI uses the ‘arithmetic mean’ which is the average with which most of us are most familiar. For example if the price of one good goes up by 10% and that of another goes up by 20%, the arithmetic mean of those increases is 15% - that is (10% + 20%) ÷ 2 . The CPI uses the geometric mean, which is calculated using multiplication. The geometric mean for the same increases is 14.9% - given by √(1.1 × 1.2) .

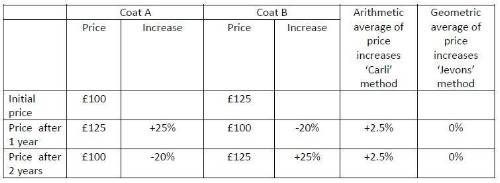

The use of the arithmetic mean to calculate inflation dates back to some of the earliest inflation statistics, calculated by the Count of Carli-Rubbi in 18th Century Venice. However, since the RPI was introduced in the 1940s the arithmetic mean has fallen out of favour due to a perception that it systematically overstates inflation. Take the following example of the calculation in the case of two similar coats.

In the first year the prices of the two coats reverse. We might think that if the two coats are close substitutes the cost of coats has not really risen, but the arithmetic average suggests it has risen by 2.5%. Worse still, when the two coats go back to their original prices in the second year, the arithmetic mean gives inflation as 2.5% again. The prices of coats are exactly where they started and yet the arithmetic mean suggests that they have gone up by 2.5% two years in a row! The geometric mean suggests that prices remained steady over the whole period. |

|

|

|

| Reinsurance Pricing Actuary, Analytics | ||

| London - £130,000 to £180,000 Per Annum | ||

| Actuary - Financial Planning & Analysis | ||

| London/Hybrid - Negotiable | ||

| Reinsurance Pricing Actuary | ||

| London - £140,000 Per Annum | ||

| Head of Capital | ||

| London - £170,000 Per Annum | ||

| ART Pricing | ||

| London - £100,000 Per Annum | ||

| Pricing Transformation Actuary | ||

| London - £130,000 Per Annum | ||

| Pricing Actuary | ||

| London - £80,000 to £120,000 Per Annum | ||

| Pensions on Divorce Startup - Flexibl... | ||

| Remote - Negotiable | ||

| SVP, Head of Reserve Forecast Analytics | ||

| Bermuda - £200,000 Per Annum | ||

| START-UP, Lead Reinsurance Actuary | ||

| London - Negotiable | ||

| Senior Actuary | ||

| London - Negotiable | ||

| Reserving Manager | ||

| London - £130,000 Per Annum | ||

| Senior Reserving Consultant | ||

| London - £100,000 Per Annum | ||

| Head of Capital | ||

| London - £180,000 Per Annum | ||

| Head of Portfolio Optimisation | ||

| London - Negotiable | ||

| Pricing Lead/Manager | ||

| London - £130,000 Per Annum | ||

| Actuary | ||

| London/Hybrid - Negotiable | ||

| Capital Actuary | ||

| London - £110,000 Per Annum | ||

| Senior Reserving Actuary | ||

| London - Negotiable | ||

| Head of Capital | ||

| London/Hybrid - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd