|

|

The Government Actuary’s Department (GAD) have now released the results of their 2020 valuation of the LGPS in England and Wales. Distinct from the triennial funding valuations with which most of us are more familiar, GAD’s valuation is carried out every four years and covers the entire Scheme. The primary purpose is to monitor changes in the cost of providing LGPS benefits and to provide assurance that these costs remain sustainable. |

By Matthew Paton, Associate and Senior Consulting Actuary at Barnett Waddingham If their valuation suggests that costs have risen or fallen significantly, then changes must be made to the Scheme to bring those costs back under control. Before we look at the main findings, it might be helpful to understand more about the origins of this process and its objectives. Please feel free to explore the interactive timeline below if you would like a recap.

2010

2011

2013 New LGPS regulations are laid to allow for the introduction of a CARE scheme. Running alongside the Treasury’s mechanism, the LGPS would also have its own, similar, “Cost Management Process” operated by the LGPS Scheme Advisory Board (the SAB). This would provide an early and more focused indication of any cost movements by including some of the unique features of the LGPS as well as being able to take some account of shifts in discount rates, allowing the SAB to recommend changes to the Scheme should they be necessary. Unlike the Treasury process where breaches require scheme changes, the SAB process operates a “must/should/may” approach to recommending changes depending on the extent of the change in costs.

2014

2018 Elsewhere, the Court of Appeal rules that the transitional protections built into the CARE reforms amount to unlawful age discrimination. The ruling is known as the “McCloud judgement”, with the Government later committing to make changes to all of the public service schemes.

2019

2020

2021

2022

2023

2024

Lessons learned Following a consultation, they announced technical changes to the operation of the Cost Control Mechanism for the 2020 valuations onwards. This reflected concerns that, after the initial 2016 breach, the mechanism was too volatile. The changes now make it less likely for a breach to occur, by excluding costs related to the legacy final salary schemes and by widening the acceptable range of costs. In addition, an “economic check” has been introduced which separately considers the impact of changes in the long-term economic outlook prior to considering any changes to the Scheme. Likewise, the SAB has introduced some analogous changes to its own process to ensure greater integration with the Treasury mechanism.

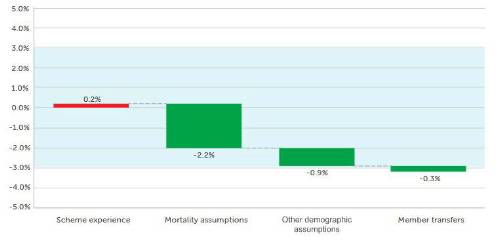

Results of the 2020 cost cap valuations Under a spruced-up methodology, the Treasury mechanism is now rather convoluted and operates in two stages. First, there is the “core cost”. This, being the main objective of the mechanism, assesses only changes in “member costs” and therefore excludes the costs of changes in long-term economic assumptions (which are instead met by employers through changes to contribution rates). The results of changes in the core cost are illustrated in the chart below. Note that, to avoid a breach, the total change must remain inside a 3% corridor, which is shaded in blue. Change in core costs

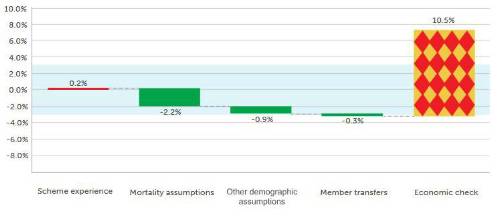

As can be seen, by far the biggest contributor is the change in mortality assumptions. Even prior to Covid, there has been a trend of declining longevity improvements in the general population which has been reflected in lower life expectancies being assumed in this valuation. Further cost savings arise due to changes to “other demographic assumptions”, such as how much pension members are assumed to exchange for cash. The chart shows that there has been a slight breach of the cost floor, which previously would have been enough to trigger improvements to scheme benefits. Under the new approach however, and this is where the second stage of the process comes in, there is an “economic check”. The idea is that if the wider economic outlook has shifted, as this may have an impact on the financial health of the local authorities who ultimately underwrite the Scheme, then it would not always be appropriate to make changes to scheme benefits. Once the impact of the economic outlook is considered, the picture could not be more different: Change in costs including “economic check”

Far from a breach of the cost floor, the economic check results in costs exceeding the cost ceiling. This is not unexpected given that the indicator of the economic outlook used in the calculation is the same as the discount rate used to set contributions in the unfunded schemes. This rate is referred to as the Superannuation Contributions Adjusted for Past Experience rate, or “SCAPE” rate for short, and has reduced enormously since the previous valuations, thereby causing spiralling contributions in those schemes. The logic of the Treasury’s economic check therefore becomes much clearer when we consider the unfunded schemes – if contributions are going up by so much then some might say it makes little sense to suggest that costs are going down and that the taxpayer is better off.

Raising the offside flag The upshot therefore is that the 2020 Cost Control Mechanism will not result in changes to scheme benefits and so, barring any further legal developments, it is a case of “as you were”. It’s worth remembering too that, unlike in the unfunded schemes, these results will have no bearing on the contributions that must be paid into the LGPS, which of course will be reviewed as part of the next triennial funding valuations. |

|

|

|

| Take the lead client-facing projects ... | ||

| Various locations - Negotiable | ||

| Choose Life! Choose a major global co... | ||

| Various locations - Negotiable | ||

| Actuarial skillset? Apply now for Snr... | ||

| South East / hybrid with travel requirements - Negotiable | ||

| Financial Risk Leader - ALM Oversight | ||

| Flex / hybrid - Negotiable | ||

| Be the very model of a modern Capital... | ||

| London - Negotiable | ||

| Pensions Actuary seeking a high-impac... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Great opportunity for Pensions Actuar... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Responsible Investing Manager - Clima... | ||

| London/Hybrid - Negotiable | ||

| Quant Strategist | ||

| London/Hybrid - Negotiable | ||

| Multiple remote longevity contracts | ||

| Fully remote - Negotiable | ||

| Multiple remote inflation hedging con... | ||

| Fully remote - Negotiable | ||

| Play a vital role in shaping a new He... | ||

| London or Scotland / hybrid 50/50 - Negotiable | ||

| Support the Longevity team of a globa... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Delve into financial risk within a ma... | ||

| Wales / South West / hybrid 1dpw office-based - Negotiable | ||

| Project-based Life Pricing Actuarial ... | ||

| South West / hybrid 2 dpw office-based - Negotiable | ||

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

| Develop your career in motor pricing | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Experience real career growth in home... | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Be at the cutting edge of technical p... | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Use your passion for innovation and t... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd