Chris Tavener - Partner at Lane, Clark and Peacock

Mortality is routinely identified as one of the major financial risks of running a defined benefit pension scheme. However, observed mortality rates themselves don’t change quickly from year to year. In my view, the financial risk associated with mortality lies in repeatedly underestimating future life expectancies, leading to unanticipated step changes in deficits, and hence contributions, when the assumption is reviewed at each triennial funding valuation.

Evidence of this can be found in the Pensions Regulator’s latest analysis of recovery plans published in December 2010. For those schemes in the latest round of valuation results analysed, the Regulator has – for the first time – knowledge of the mortality assumptions used at two successive valuations. The average inter-valuation increase in life expectancy for a current pensioner aged 65 was 1.4 years – quite a hefty increase given this is an average across a thousand pension schemes.

So, is life expectancy still being underestimated? With the vast amounts of research and time dedicated to setting this assumption, I would like to hope not.

A key step forward has been that more thought has gone into setting the mortality assumption having regard to the characteristics of the membership of the scheme. When setting the base rates of mortality for a scheme’s valuation, it is increasingly standard practice for a standard base table should be adjusted (or “rated”) to allow for the differences between the characteristics of the scheme’s members and the characteristics of the persons on which the mortality experience of the standard base table has been based upon.

It is interesting to note that the Regulator’s analysis of recovery plans reveals that that the proportion of schemes using an unadjusted standard table is falling, down to 51% of scheme from 70% three years previously.

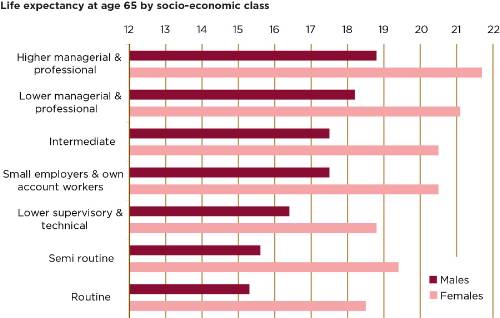

In respect of current rates of mortality, socio-economic class is a big differentiator and a factor I believe should be taken into account. Research recently published by the Office for National Statistics (in their Spring 2011 edition of Health Statistics Quarterly) contrasts the life expectancies of people in different socio-economic classes (see chart 1). This highlights that the average life expectancy at age 65 for men doing routine jobs, such as car park attendants, is 3.5 years less that for those in professional/higher managerial roles such as lawyers. Perhaps it is not surprising that the Government has targets to reduce this inequality.

When looking at how mortality rates may develop in the future, there are numerous alternative projections. The latest projection model has been published by the CMI. It is definitely a step forward, and is far more credible than the commonly used medium or long cohort projections which were based solely on male experience and, when first published in 2002, were described as interim and “a work in progress” (with the longer-term aim to have a rather more considered and robust method).

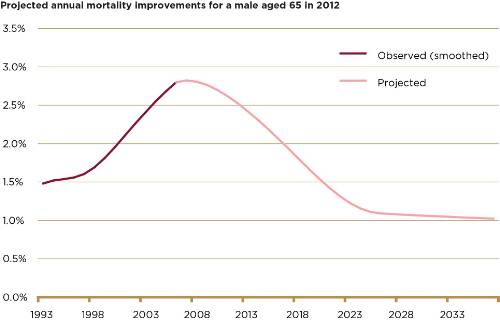

However, the new CMI model still has shortcomings. My biggest reservation is that the CMI chose to construct the model such that it has no regard for the recent trend in observed improvements. Consequently, rather than a smooth transition from the observed improvements to the future projection, there can be a rather marked discontinuity – with the recently observed improvements trending upwards, switching abruptly to projected improvements trending downwards (see chart 2).

Although the financial impact may be minimal, the projection can look unrealistic when presented to a board of pension scheme trustees. This shortcoming can be solved by moving away from using the model’s core parameters, but the complications of describing the non-core parameters in, say, a valuation report, unfortunately makes this an impractical solution in the real world.

I can still see the CMI projections catching on, and becoming the norm over the next year or so as the medium and long cohort projections start to look even more outdated.

How will the assumption for future improvement projections be chosen in several years’ time? I would like to see conversations with scheme trustees and sponsoring employers move away from a debate on which “underpin” is suitable, or what “long-term rate” to use, and be more driven by potential scenarios for the future. In particular, a better understanding of the risks and potential financial implications may be gained by considering scenarios for how major causes of death could develop over time. This type of discussion can be far more intuitive to a trustee/finance director than discussing the parameters of a mathematical model.

For instance, a news story seen by a trustee or finance director may be about the progress towards finding a “cure for cancer”. Since around a third of all current deaths of males over age 65 is registered as having cancer as the underlying cause (based on data published by the Office for National Statistics), a cure for all cancers could lead to a material increase of a couple of years in assumed life expectancies.

Ultimately the choice of the mortality assumption, and in particular the allowance for future improvements, is very subjective – there is no correct answer. We need to be up front that we do not know how long we are all going to live with any degree of certainty. The selection of an assumption needs to be pragmatic, justifiable, easily understood, evidence-based and, importantly, up-to-date. This will help ensure that regular reviews of the mortality assumption only lead to fine-tuning, and avoids unanticipated step changes which can lead to unwelcome financial pressures on schemes and their sponsors.

|

Chart 1: Life expectancy at age 65 by socio-economic category

|

|

|

|

Source: Office for National Statistics, Health Statistics Quarterly, Spring 2011

|

|

Chart 2: Projected mortality improvements for a male 65 in 2012

|

|

|

|

Source: CMI 2009 model with core parameters and long-term rate of 1.0% pa

|

|