With many pundits predicting a ‘dash for cash’, Partnership asked over-40s what proportion of their pension pots they intended to take in cash when they retired and they typically intended to take 27% - only marginally higher than the tax free allowance. In addition, while 45% were supportive of the freedom to cash in pension pots, 34% say that if people ‘blow their cash’ they should not expect state support.

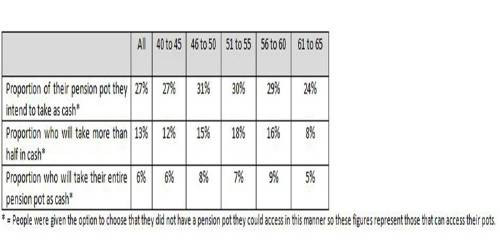

Pension Pot Intentions:

Those between the ages of 51 to 55 were most likely to take more than half of their pot as cash at retirement (18%) but those aged 46 to 50 intended to take the largest proportion as cash (31%). Those aged 56 to 60 were most likely to take their entire pension post as cash (9%).

When asked why they wanted part of their pots as cash, 45% said that they wanted to keep it in a bank account for treats, 18% wanted to spend it on a holiday or something to celebrate retiring and up to 31% intended to repay borrowing (17% - repay debt and 14% repay mortgage). Replacing their car (16%) or household appliances were also a priority (11%).

Freedom with Implications:

While 45% of 16 to 75 year olds said that people should be able to spend their pension as they saw fit as ‘it is their own money, others were more cautious. Indeed, 34% said that if someone takes their pension as cash and ‘blows it’ then they should not be able to ask for state support and 18% said that only those with medical conditions or have retired should be able to take cash out of their pension at 55.

Interestingly, people who are over-65 years old are least likely to be supportive of benefits for those who take their pension cash and spend it (44%) compared to the under-35s (25%) who arguably will be funding this deficit with their taxes. This may seem counter-intuitive but may well be because the over-65s have already made irreversible choices around their own pensions and the under-35s are thinking about their own retirement aspirations.

Andrew Megson, Managing Director of Retirement, said:

“While some have predicted a dash for cash following the introduction of the pension freedoms, most people appear to be intending to take only marginally more than they might have before. They also generally appear to be spending the cash they take out on sensible choices such as the repayment of debt, replacing their car or appliances and putting it aside for incidental costs in retirement.

“Arguably withdrawing money to put into a savings account can have tax implications but building a nest egg for expenses is certainly sensible. When questioned about the freedoms, it is interesting to note that while 45% said that people should be able to do what they want with their money, 34% were concerned about the wider picture and said that if people ‘blew their cash they should not be able to ask for state support.’

“It appears that while people are keen on the idea of more pension freedom, they are still relatively prudent in their approach to spending their pots – and expect others to be as well.”

|