|

|

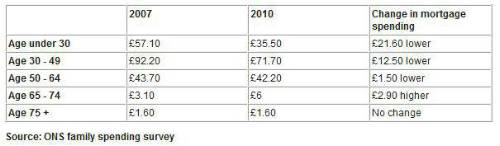

Official statistics released this week, seem to indicate that, rather than acting as a stimulus, Bank of England policy may have had a detrimental impact on the UK's economic growth. Dr Ros Altmann, Director-General of Saga, who has long warned of the dangers of the Bank of England's monetary policy, cautions that a reassessment of the stance of monetary policy is urgently required: Today's growth figures should by no means be seen as a sign that monetary measures have aided our economic recovery. In fact, the ONS National Wellbeing report released earlier this week indicates that Quantitative Easing may have led to a slower economic recovery than we experienced during both the 1979 and 1990 recessions. While unemployment has not been as severe as previous recessions, we have seen incomes drop and then fall further rather than recovering as would usually be expected. Low interest rates have reduced people's savings income and the rising cost of living has decimated their spending power. QE has caused a severe drop in incomes compared to previous recessions The ONS data show that after the 1979 and 1990 recessions, the economy and household incomes recovered well from one and half years on (six quarters after the downturn). That would mean from third quarter 2009 the UK should have begun a good recovery. In fact, however, this time round, growth remained depressed and household incomes fell again from 2010 onwards. This was the period when QE was being introduced and, despite the Bank of England's measures, the economy continued to weaken. QE did not generate recovery In the early stages of the recession interest rates reached historic lows and mortgage interest payments fell, meaning many householders' disposable incomes rose as a result of lower mortgage payments. This helped through to mid 2009, however this effect wore off after 2009 and QE failed to provide any new stimulus. Indeed, it seems borrower's over indebted positions did not allow them to keep spending as inflation picked up while QE then kicked in and damaged incomes of older households who were not heavily in debt. As older people have low or no mortgage debt they did not benefit from the cuts to mortgage rates. Generational effects of mortgage rate cuts: Average mortgage spending per week:

Inflation was cause of falling incomes As the ONS itself says, "This fall in household actual income per head was primarily due to prices going up at an increasing rate over most of the period." In other words, QE's boost to inflation seems to have damaged household incomes in a way that had not happened after previous recessions. ONS Figure 3: net national income per head during three recessions Start of recession 4 ½ years later ONS Figure 4: Real household actual income per head during two recessions Start of recession 4 ½ years later Inflation has damaged economic wellbeing and growth The ONS says that "during 2011 high inflation was driven by rises in food prices, utility bills and fuel prices". The increase in prices eroded the growth of household incomes, meaning real household actual incomes fell. Because inflation was driven by the cost of essentials, it hit poorer and older people much harder than average. This will have damaged their spending power and made them feel much poorer. Monetary policy operated like a tax increase on savers In addition, older households also suffered severe falls in their savings income as the Bank of England kept interest rates low. Coupled with high inflation, this meant that savers income fell. Cutting older people's incomes is like a tax increase on older generations. The ONS report states: "Until May 2008 the CPI remained between one and three per cent, and the interest paid on savings was higher. However, through 2008 inflation continued to climb month on month until reaching a peak of 5.2 per cent in September. Meanwhile, the Bank of England cut the official bank rate to an unprecedented low of 0.5 per cent, resulting in interest rates paid on savings falling. Real loss to savers was at its most pronounced in Sept 2011 when CPI reached its peak of 5.2%." The toxic combination of low interest rates and high inflation had disastrous effects on people's disposable incomes and on their spending power hindering economic growth and leading to a weaker economy. The ONS report shows how interest rates on deposits and savings accounts fell sharply, even as inflation was high, and rates remained low while inflation soared again. This left older generations approaching or in retirement facing significantly reduced nominal and real incomes. The consequence of this, counter to Bank of England expectations of savers increasing their spending, was reduced consumption and weaker growth. ONS Figure 9: Inflation and interest rates paid on savings This recession has transferred income from old to young and from middle incomes to the rich In fact, monetary policy has redistributed national income and wealth from older to younger generations without any democratic debate. The ONS points out that "A high rate of inflation reduces the real value of wealth held in cash terms" This is important because the Bank of England recent report showed that 90% of savers money is in cash. Therefore the higher the rate of inflation, the greater the reduction in the real value of wealth held in cash. Therefore the rate of inflation relative to the rate of interest has an important impact on the distributional effects of economic well-being; The ONS goes on to say "the rate of inflation relative to the rate of interest has an important impact on the distributional effects of the economic wellbeing relatively." The ONS itself also states "a relatively high inflation rate redistributes net wealth from savers to debtors". And relatively "high inflation rate can redistribute wealth from the older to the younger generation."

It is essential that the Bank of England holds back on further gilt-buying in November. Quantitative Easing (QE) is a drastic policy experiment that may have been worth trying in 2009 to avoid depression but even as the economy was recovering and inflation was above target, the Bank carried on buying more gilts. With inflation pressures rising again, the Bank should more carefully assess the effects of QE before instigating any more measures. |

|

|

|

| Take the lead client-facing projects ... | ||

| Various locations - Negotiable | ||

| Choose Life! Choose a major global co... | ||

| Various locations - Negotiable | ||

| Actuarial skillset? Apply now for Snr... | ||

| South East / hybrid with travel requirements - Negotiable | ||

| Financial Risk Leader - ALM Oversight | ||

| Flex / hybrid - Negotiable | ||

| Be the very model of a modern Capital... | ||

| London - Negotiable | ||

| Pensions Actuary seeking a high-impac... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Great opportunity for Pensions Actuar... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Responsible Investing Manager - Clima... | ||

| London/Hybrid - Negotiable | ||

| Quant Strategist | ||

| London/Hybrid - Negotiable | ||

| Multiple remote longevity contracts | ||

| Fully remote - Negotiable | ||

| Multiple remote inflation hedging con... | ||

| Fully remote - Negotiable | ||

| Play a vital role in shaping a new He... | ||

| London or Scotland / hybrid 50/50 - Negotiable | ||

| Support the Longevity team of a globa... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Delve into financial risk within a ma... | ||

| Wales / South West / hybrid 1dpw office-based - Negotiable | ||

| Project-based Life Pricing Actuarial ... | ||

| South West / hybrid 2 dpw office-based - Negotiable | ||

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

| Develop your career in motor pricing | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Experience real career growth in home... | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Be at the cutting edge of technical p... | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Use your passion for innovation and t... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd