|

|

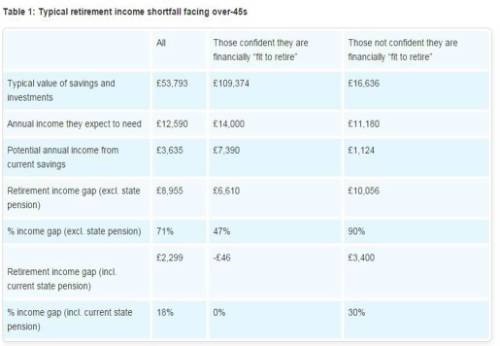

The typical working over-45 year old faces a £8,955 annual retirement income gap based on their current savings and investments – leaving them to rely heavily on a state pension that will still leave them short, the latest Aviva Real Retirement Report shows. |

The report reveals that over-45s, who are not yet retired, typically expect to need an annual income of £12,590 from their savings and investments when they retire.

But Aviva’s analysis shows their typical current savings and investments only amount to £53,793, which would deliver income of £3,117 a year if an annuity is bought or £3,635 each year if invested in a drawdown plan over 25 years¹.

This means the typical person only has enough private savings to finance 29% of their target income: leaving them with a potentially crippling £8,955 retirement income gap every year before the state pension is taken into account.

Today’s average state pension income of £6,656² would bring their annual shortfall down to £2,299 in retirement. It means that the typical person is relying on the state pension to fund more than half (53%) of their expected retirement income. But not even the new flat rate state pension – offering a maximum of around £7,800 to those who will qualify for it from April 2016 – will fully bridge the gap between their expectations and reality.

Even those over-45s who are confident and have the largest pots (£109,374) can only rely on this sum to provide an annual income of £7,390 over a 25 year retirement. This is £6,610 short of the £14,000 a year they expect to need, although their confidence may reflect a degree of awareness that the state pension will at least make up the difference.

Saving just £86 extra a month can close the remaining gap

Aviva’s findings are especially concerning for those over-45s who are closer to retirement and have less of a window to grow their savings. Worryingly, 29% have not even thought about how much retirement income they will need. Those aged 55-64 are more likely to have neglected the issue (34%) than 45-54s (21%) – despite having less time to act.

However, Aviva’s analysis offers hope to over-45s by showing how a modest boost to savings habits can help them build an extra pot of £42,000: an amount which, in today’s money, would bridge the remaining £2,299 retirement income gap once the state pension is added to their existing funds.

Assuming they wanted to retire at 67, a 45 year old paying the basic 20% rate of tax could reach the target of £42,000 by increasing their monthly savings by £86, or just £64 for a higher (40%) taxpayer.³

Even if they delayed taking action until the age of 55, they could reach the £42,000 target by 67 by saving an extra £179 a month (for basic taxpayers) or £134 (for higher taxpayers). One route to saving more is by increasing pension contributions, which will particularly benefit those people in a workplace scheme where their employer also contributes. Cutting back on non-essential spending or taking on extra work are other routes to higher savings.

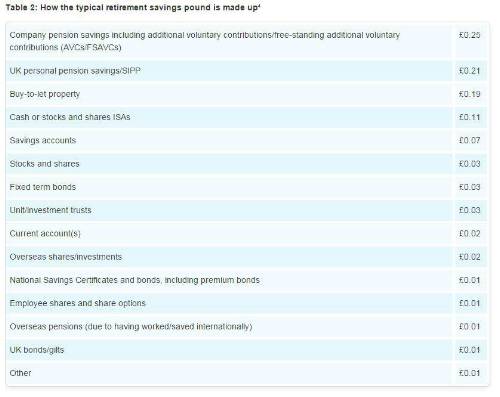

Pensions ‘power boost’ makes up 46p in every £1 saved for retirement

Examining the typical £53,793 pot among over-45s confirms that pensions are the ‘power boost’ in savings portfolios. These account for 46p in every £1 saved, including 25p in a company pension and 21p in a personal pension or Self-Invested Personal Pension (SIPP). In contrast, savings accounts deliver 7p in every £1 and current accounts just 2p.  However, with auto-enrolment only just reaching smaller companies, two in five over-45s have a company pension (43%). Fewer still have a personal pension or SIPP (30%): far below the 82% with current accounts and 70% with savings accounts.

Having savings accounts, ISAs and company pension savings are key indicators of feeling confident about retirement finances. ISAs contribute 11p for every £1 saved by over-45s, but again less than half (46%) use this method of saving.

Buy-to-let (BTL) property contributes 19p in every £1 overall: almost as much as ISAs, savings accounts and current accounts combined (20p). But this is an expensive venture: among those who have a BTL property, the typical investment is £126,440.

Clive Bolton, Managing Director, Retirement Solutions, Aviva UK Life, said:

“These findings should encourage every person still in work to think hard about their retirement finances and which group they fall into: the reasonably fit to retire, the potentially fit to retire or the currently unfit to retire. The pension freedoms have broadened people’s financial options in later life – but they don’t guarantee freedom from responsibility when it comes to better planning and improving savings habits.

“As things stand, the vast majority of people are in danger of being left short-changed by insufficient savings pots, but with the addition of the state pension, the gap is narrow enough to enable them to take action to close it completely.

“Finding additional ways to supplement their savings, such as increasing pension contributions while they are in work, working for longer or taking on a part-time job in retirement, may be enough to help them reach their target income.”

Tackling the retirement income shortfall – what should consumers consider?

1. Understand what your total savings pot will provide as retirement income and how this measures up to your expectations. 2. Consider the diversity of your investments – could you get better returns by spreading your money around more? 3. Commit to pensions and make the most of personal and employer contributions. 4. Consider steps you can take to increase your savings – whether it is increasing pension contributions, working for longer, or taking on a part-time job in retirement. 5. Take an active interest in how your savings and investments are performing – don’t let apathy rule your future. 6. Act sooner rather than later to adjust your strategy and contribute more whenever you can. |

|

|

|

| Take the lead client-facing projects ... | ||

| Various locations - Negotiable | ||

| Choose Life! Choose a major global co... | ||

| Various locations - Negotiable | ||

| Actuarial skillset? Apply now for Snr... | ||

| South East / hybrid with travel requirements - Negotiable | ||

| Financial Risk Leader - ALM Oversight | ||

| Flex / hybrid - Negotiable | ||

| Be the very model of a modern Capital... | ||

| London - Negotiable | ||

| Pensions Actuary seeking a high-impac... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Great opportunity for Pensions Actuar... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Responsible Investing Manager - Clima... | ||

| London/Hybrid - Negotiable | ||

| Quant Strategist | ||

| London/Hybrid - Negotiable | ||

| Multiple remote longevity contracts | ||

| Fully remote - Negotiable | ||

| Multiple remote inflation hedging con... | ||

| Fully remote - Negotiable | ||

| Play a vital role in shaping a new He... | ||

| London or Scotland / hybrid 50/50 - Negotiable | ||

| Support the Longevity team of a globa... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Delve into financial risk within a ma... | ||

| Wales / South West / hybrid 1dpw office-based - Negotiable | ||

| Project-based Life Pricing Actuarial ... | ||

| South West / hybrid 2 dpw office-based - Negotiable | ||

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

| Develop your career in motor pricing | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Experience real career growth in home... | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Be at the cutting edge of technical p... | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Use your passion for innovation and t... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd