-

Deficits will not resolve themselves, so now is the time to focus on solutions

-

15 years is a more realistic timeframe to repair pension scheme deficits, compared to current average 9-10 years

-

Gilt yield based measurement of pension liability value may not represent reality

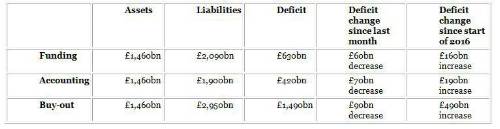

PwC’s Skyval Index, based on the Skyval platform which individual pension funds use, provides an aggregate health check of the UK’s c6,000 DB pension funds.

The current Skyval Index asset, liability and deficit levels of DB pension funds are:

Notes on the three measures:

• Funding: the value of liabilities used by pension fund trustees to determine company cash contributions, calculated on a scheme-specific basis for each pension fund agreed between the trustees and sponsor.

• Accounting: the value of liabilities shown in company accounts, based on discounting future pension obligations using

AA-rated corporate bond discount rates. Pension decision-makers should not rely on the accounting measure, cited by many commentators, to inform their management decisions. Accounting numbers are calculated according to prescribed standards, and are not designed to be tailored to individual pension fund circumstances. They serve a purpose for historic formal financial reporting in accounts, but are not in isolation a good basis for deciding the best future strategy for a pension fund's assets and liabilities.

• Buy-out: the value an insurer would typically place on the fund's liabilities, which depends on prevailing market terms for these kinds of transactions. It is a hypothetical scenario for all pension fund to buy out their total liabilities in one go as there is not enough capital market capacity to support this.

Raj Mody, partner and PwC’s global head of pensions, said: “The funding deficit has improved by £60bn this month due to a combination of asset and liability value movements during another volatile month.

“Slight improvements in gilt yields have contributed to the apparent deficit reduction, but liability measurement by gilt yields does not necessarily represent reality, given pension liabilities are mainly affected by longevity and inflation.”

PwC advises pension fund decision-makers to consider a range of solutions which do not focus solely on short-term volatility but which address the underlying challenge.

Raj Mody, added: “Companies and trustees should first look at pensioner liabilities and consider taking these off their balance sheet.

“Otherwise they are gradually turning into an annuity provider, which would seem odd, unless that is their business. Instead, they could take steps to avoid their pre-retirement liabilities turning into post-retirement liabilities.

“Insurance at the right price could be an option as new technology provides early visibility of scheme-specific pricing. Schemes can carry out a transaction as and when there is a favourable pricing window.

“There are plenty of ways to reshape and optimise liabilities in the run-up to members’ retirement. Only offering one option at retirement – to swap a quarter of your pension for a lump sum – is outdated. In this age of freedom and choice, with possibilities such as flexible retirement options, a range of more modern choices can be presented to savers.”

PwC advocates a review of how pension deficits are repaired and how pension investment strategies are formulated, to give trustees a better chance of being safer, sooner. PwC’s past research showed deficit repair periods ranging from 1 to 21 years, with the average being 9 years.

Raj Mody, concluded: “Some companies may want to consider extending the length of time taken to repair the deficits, which will mitigate the sometimes artificial adverse consequences of current low gilt yields, if pension funds are still stuck with outdated measurement methods for their deficit.

“Most pension funds have generally become conditioned to expect to repair deficits in shorter than 10 years, albeit many funds have to treat that as a rolling period each time they review the position. Financial planning meetings must feel like Groundhog Day.

"Ten years may have felt about right in historical economic circumstances, but a timeframe closer to 15 years on average may be more realistic. This provides more time to see if the deficit really needs to be repaired with cash, by allowing asset returns to pay off over a longer period, and allows views on life expectancy to settle. In any case, it should not be a one-size-fits-all answer but a scheme-specific consideration.”

|