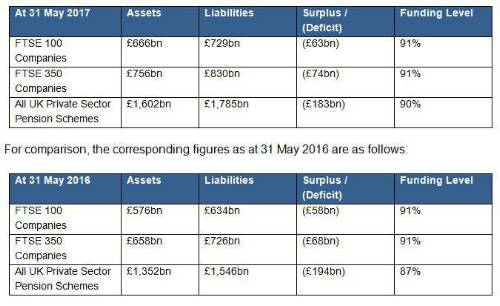

As at 31 May 2017, JLT estimates the total DB pension scheme funding position as follows

Charles Cowling, Director, JLT Employee Benefits, comments: “As Britain prepares to go to the polls, we note that pensions have not been a key battleground for the main political parties - or at least not the issues surrounding hard pressed defined benefit (DB) pension schemes in the private sector.

“However, for many companies the management of their DB pension liabilities is their single biggest headache. The Pensions Regulator, in its latest annual funding statement, just published, has highlighted the issue of fair treatment between pension schemes and shareholders. In particular, it has stated an expectation that where dividends are higher than deficit recovery contributions, it expects to see a ‘relatively short recovery period’. This is going to cause some tension in boardrooms and trustee meetings when it comes to agreeing how deficits revealed by 2017 actuarial valuations are going to be financed.

“This tension will not be eased by the continuing likelihood of the IASB (International Accounting Standards Board) making a technical amendment to the accounting standard IFRIC14, which has the potential to increase very significantly the liability that a company must show in its accounts for its DB pension scheme.

“So, while markets are calm at present and deficits are relatively stable, DB pension schemes still have much to worry companies and shareholders. Moreover, with a General Election and Brexit looming there is still the potential for markets to add to these woes. Companies would do well therefore to look for opportunities to decrease or settle DB liabilities. For those few companies still allowing employees to earn additional DB benefits, 2017 is likely to be the year that they finally pull plug on this once much treasured and ubiquitous employee benefit.”

|