|

|

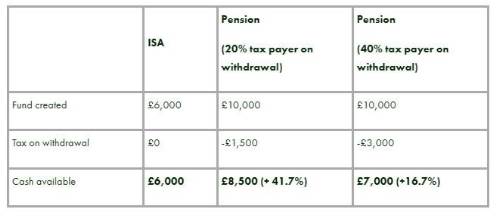

Over 50s should prioritise pensions over ISAs because of tax relief and flexibility. Tax relief can boost returns by up to 41.7% for higher rate taxpayers and 25% for basic rate taxpayers. 4.5million 55-64-year-olds have ISAs holding an average amount of £29,800 |

Millions of investors in their 50s and 60s could be thousands of pounds better off prioritising pensions over ISAs as the end of the tax year looms on April 5. Latest figures show 4.5million people in the UK aged between 55-64 have ISAs worth an average of £29,80. While money can normally be taken from ISAs at any time, flexible pension rules mean investors can access pensions from 55-years-old (57 from 2028) taking the money as lump sums if they wish. And the impact of pension tax relief means returns could be boosted by up to 41.7% for higher rate taxpayers and 25% for basic rate taxpayers. Sean McCann, Chartered Financial Planner at NFU Mutual, explained: “As the end of the tax year approaches, many people will be topping up ISAs in the knowledge that they can access the funds if they need to. “But once you reach 50 and over, the point at which you can take money from your pension draws closer. “The tax relief available from pensions can give a significant boost to returns, particularly if you’re going to be in a lower tax band when you take the money out. "Latest figures show 4.5million people aged between 55 and 64 hold ISAs with an average value of nearly £30,000, but many of them could be better off topping up their pension and claiming the tax relief. “Unlike ISAs, money held in pensions is normally exempt from inheritance tax. For those that can afford to it can make sense for pensions to be the last investment they access in retirement.” Higher rate taxpayer example:

Over 55 with £6,000 to invest

|

|

|

|

| Take the lead client-facing projects ... | ||

| Various locations - Negotiable | ||

| Choose Life! Choose a major global co... | ||

| Various locations - Negotiable | ||

| Actuarial skillset? Apply now for Snr... | ||

| South East / hybrid with travel requirements - Negotiable | ||

| Financial Risk Leader - ALM Oversight | ||

| Flex / hybrid - Negotiable | ||

| Be the very model of a modern Capital... | ||

| London - Negotiable | ||

| Pensions Actuary seeking a high-impac... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Great opportunity for Pensions Actuar... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Responsible Investing Manager - Clima... | ||

| London/Hybrid - Negotiable | ||

| Quant Strategist | ||

| London/Hybrid - Negotiable | ||

| Multiple remote longevity contracts | ||

| Fully remote - Negotiable | ||

| Multiple remote inflation hedging con... | ||

| Fully remote - Negotiable | ||

| Play a vital role in shaping a new He... | ||

| London or Scotland / hybrid 50/50 - Negotiable | ||

| Support the Longevity team of a globa... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Delve into financial risk within a ma... | ||

| Wales / South West / hybrid 1dpw office-based - Negotiable | ||

| Project-based Life Pricing Actuarial ... | ||

| South West / hybrid 2 dpw office-based - Negotiable | ||

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

| Develop your career in motor pricing | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Experience real career growth in home... | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Be at the cutting edge of technical p... | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Use your passion for innovation and t... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd