As at 31 March 2017, the PPF was 121% funded with £6.1bn of reserves. The impact on the PPF’s reserves of Carillion’s DB schemes falling into the PPF is likely to be lower than £0.9bn, as the PPF doesn’t fund itself on the same assumptions as those used in a s179 valuation – which is used to determine the PPF levy for individual schemes – and there may also be some debt recovered.

According to the PPF 7800 Index, at the end of December 2017, the 5,588 PPF-eligible DB schemes had an aggregate deficit of £103.8bn. Of those 5,588 schemes, 3,710 schemes were in deficit to the tune of a combined £210bn. On the face of it, this points towards a bleak future, prompting the CEO of a large independent financial advisory firm to ask: “how many more big hits can the PPF take?”

But what these snapshot figures hide, is that the PPF continues to go from strength-to-strength, and the financial position of the UK’s 6,000 DB schemes remains healthy.

For example, the PPF’s reserves at 31 March 2017 were £2bn higher than the previous year, as a result of strong investment performance, income from levies and lower than expected claims volumes, and the PPF remains on target to be “financially self-sufficient” (or levy-free) by 2030. In addition, according to the PPF 7800 Index, the number of DB schemes in surplus on a s179 basis has increased from 1,482 out of 5,794 (or 26%) at 31 March 2017, to 1,878 out of 5,588 (or 34%) at 31 December 2017.

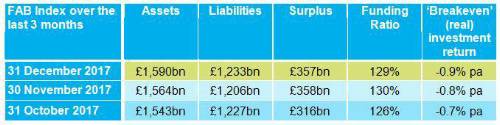

First Actuarial’s Best estimate (FAB) Index – which provides the best estimate position of the UK’s 6,000 DB pension schemes calculated using the best estimate expected return on the assets held by those schemes – remained strong over December, with a month-end surplus of £357bn, and a healthy 129% funding ratio.

First Actuarial Partner Rob Hammond said: “It is a sad day for the 20,000 UK employees of Carillion whose future remains uncertain. But it is important that Carillion’s pension scheme members (and members of other defined benefit schemes) know that their pensions are protected.

“The PPF can take the strain of Carillion’s £0.9bn section 179 shortfall – the actual impact on the PPF will be lower than £0.9bn – and it is well-equipped to cope with any future insolvencies. The financial position of the UK’s remaining 6,000 defined benefit schemes will also improve over time as companies continue to plug funding deficits.

“So, we urge members not to fall for scaremongering from unscrupulous advisers using situations like this to encourage people to transfer out of their own valuable, defined benefit schemes.”

The technical bit…

Over the month to 31 December 2017, the FAB Index remained stable, with the surplus in the UK’s 6,000 defined benefit (DB) pension schemes falling slightly from £358bn to £357bn.

The deficit on the PPF 7800 Index worsened over December from £87.6bn to £103.8bn.

These are the underlying numbers used to calculate the FAB Index.

The overall investment return required for the UK’s 6,000 DB pension schemes to be 100% funded on a best estimate basis – the so called ‘breakeven’ (real) investment return – has fallen to minus 0.9% pa. That means the schemes need an overall actual (nominal) return of 2.7% pa for the assets to meet the liabilities.

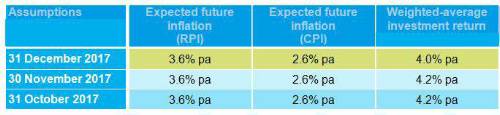

The assumptions underlying the FAB Index are shown below:

|