|

|

There have been few periods this century where private equity markets didn’t outperform public market indices over the long-term (as measured by ten-year rolling returns). Whilst this trend may continue, there are several challenges currently facing the asset class which could reduce the margin of outperformance going forwards. For investors such as family offices and endowments, who typically have significant private equity exposures, is this risk being managed appropriately? |

We expect to see a rise in the dispersion of private equity manager returns, driven by the heightened expertise required to navigate the challenges and reduced expectation of strong market beta returns seen in the past. Investors should remain mindful of the prevailing headwinds within the asset class and seek assurance that their chosen manager possesses the capability to generate returns that justify the illiquidity and governance complexities. "As always, there is uncertainty around the future direction of travel, but pockets of opportunity are likely to continue to exist within the private equity market." Below, we set out how to overcome current challenges and leverage potential opportunities in a complex, changing landscape. Navigating challenges

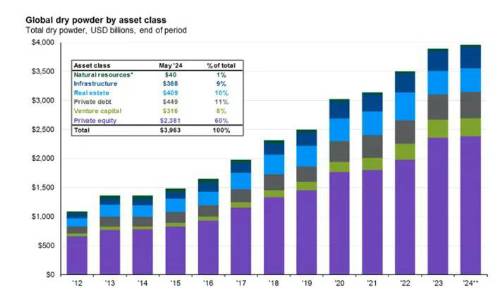

Too much dry powder?

This has created significant competition (and hence rising prices) for high quality assets, alongside increasing pressure for private equity managers to invest in lower-quality assets in the face of looming investment period deadlines. Source: Preqin, J.P. Morgan Asset Management. Dry powder refers to committed but uninvested capital. Fundraising categories are provided by Preqin. *Natural resources includes energy, timberland, agriculture and farmland, metals and mining, water, and diversified business. **Data updated through May 31, 2024. Percentages may not sum to 100 due to rounding.

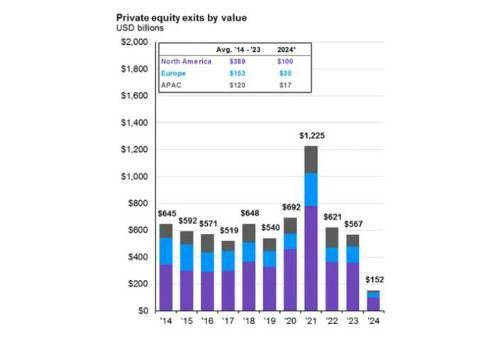

Subdued market exit Market uncertainty over the recent past effectively closed the Initial Public Offer (IPO) market and higher interest rates from central banks meant Merger & Acquisition (M&A) activity would be costly and was put on pause.

Indications suggest that the market is beginning to ease its congestion. This is due to a combination of managers being more open to accepting lower prices and a reduction in spreads within the private credit market, thereby opening financing options. Whether this represents a temporary unclogging remains to be seen. In any case, the trend for a greater proportion of companies remaining privately-owned seems set to continue. Source: Preqin, J.P. Morgan Asset Management. Exits include Bankruptcy/Write-off, IPO, Private placement/follow on, sale to management, secondary buyout, secondary stock purchase, trade sale, unspecified exit. *Data for the year 2024 is as of May 31, 2024.

Merry-go-round

Increased financing costs While certain private equity managers have weathered periods of elevated rates before, such as those in the 1990s, this current environment may still erode returns in the private equity sector. It begs the question of whether the premium above private credit justifies assuming the additional risk.

Additional lending facilities Although these facilities can help from a capital-raising, liquidity or expected return perspective, they may also introduce additional leverage to a private equity fund in a somewhat opaque manner and sometimes without investors’ knowledge.

Leveraging opportunities

Go long

Choose your vintage wisely As a result, investors may wish to think carefully before automatically redeploying capital into their managers’ latest fund vintage, and instead focus on those managers which they feel are best suited to weathering the current market challenges.

Use secondary market Although secondary market discounts may be expected to reduce slightly from their current (close to historic high) levels, the market continues to develop and it remains a buyer’s market. Indeed, this is also the case in a wide range of private markets, not just private equity. We believe that the challenges outlined above are in no way insurmountable, and private equity continues to offer the potential for good returns going forward.

What’s next?

Managers holding onto assets for longer; But despite these issues, we still expect the asset class to provide good returns in future, albeit likely being harder to find and taking longer to achieve. Good opportunities remain for investors able to deploy capital for the long-term with high quality managers. Currently, secondary markets may create better entry opportunities, enabling investors to maximise their risk-adjusted return potential. |

|

|

|

| Take the lead client-facing projects ... | ||

| Various locations - Negotiable | ||

| Choose Life! Choose a major global co... | ||

| Various locations - Negotiable | ||

| Actuarial skillset? Apply now for Snr... | ||

| South East / hybrid with travel requirements - Negotiable | ||

| Financial Risk Leader - ALM Oversight | ||

| Flex / hybrid - Negotiable | ||

| Be the very model of a modern Capital... | ||

| London - Negotiable | ||

| Pensions Actuary seeking a high-impac... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Great opportunity for Pensions Actuar... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Responsible Investing Manager - Clima... | ||

| London/Hybrid - Negotiable | ||

| Quant Strategist | ||

| London/Hybrid - Negotiable | ||

| Multiple remote longevity contracts | ||

| Fully remote - Negotiable | ||

| Multiple remote inflation hedging con... | ||

| Fully remote - Negotiable | ||

| Play a vital role in shaping a new He... | ||

| London or Scotland / hybrid 50/50 - Negotiable | ||

| Support the Longevity team of a globa... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Delve into financial risk within a ma... | ||

| Wales / South West / hybrid 1dpw office-based - Negotiable | ||

| Project-based Life Pricing Actuarial ... | ||

| South West / hybrid 2 dpw office-based - Negotiable | ||

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

| Develop your career in motor pricing | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Experience real career growth in home... | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Be at the cutting edge of technical p... | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Use your passion for innovation and t... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd

By Michelle Bellwood FIA, Principal and Senior Investment Consultant and Amy Taylor, Senior Research Analystfrom Barnett Waddingham

By Michelle Bellwood FIA, Principal and Senior Investment Consultant and Amy Taylor, Senior Research Analystfrom Barnett Waddingham