Philip Hammond appeared to avoid throwing any deliberate hand grenades this Autumn Statement but reducing the Money Purchase Annual Allowance –the amount you can save into a pension once you have taken money out of it – may turn out to be more explosive than the Chancellor intended.

There was no tinkering with the triple lock or pensions tax relief despite speculation from some commentators ahead of the statement that there might be (although the triple lock looks to be under threat after 2020 – Hammond passing the buck to a future Chancellor). When it came to tax and savings, the Chancellor majored on salary sacrifice and launching a new corporate savings bond squarely aimed at the so-called JAMs.

But the Government’s move to reduce the money purchase annual allowance from £10,000 to £4,000 for the over-55’s fails to consider the shift in working patterns taking place in the UK.

Platforum’s recent consumer research Consumer Insights: Facing an Uncertain Retirement shows that over a third of working age adults have no clear idea of when they will retire. 16% of working age adults expect that there will be a date when they stop working but don’t imagine that they will stop working completely, up from 13% in 2015. This percentage rises significantly to 26% of working age active private investors. Clearly, the percentage of working age adults who expect to continue working in some form past retirement age is rising.

We call this segment the grey gliders, the group of people who are not fully retired but who are not working full time either. In 2015, ONS figures suggested that 12% of UK adults were working beyond the state pension age, up by a quarter from 2001. Reducing the money purchase annual allowance for pension savers that have opted to take some of their pension savings will hit this group.

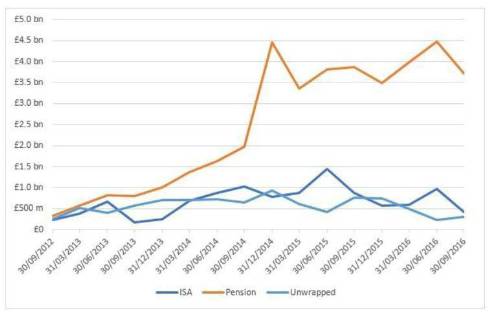

Our latest adviser platform research for Q3 shows that net sales into pension wrappers are up again quarter on quarter at a staggering 82% of net sales. But it hasn’t always been so. Flows to pension wrappers on adviser platforms started to spike in 2014, when the pension freedoms were announced. As this chart shows, they have continued to rise suggesting that the pension freedoms has improved confidence in pension saving.

When the pension freedoms were introduced, we asked savers what they thought: “Pensions have had such a bad name in the past, now you are a bit more in control of your money which is a much much better thing.”

As one saver put it following the pension reforms “I’d rather be in control of my own destiny.” Philip Hammond’s latest measure removes some of that freedom; a backwards step for pension savers and a kick in the teeth for grey gliders.

|