By Andrew Downes, Senior Investment Consultant, Stamford Associates

While heightened market volatility may continue for some time, it is important to be reminded of one’s long-term strategic objectives and determine what needs to be done to get the original long-term strategic asset allocation back on track.

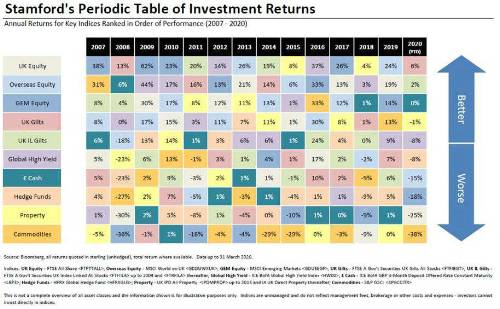

Rationale for Rebalancing

The strategic asset allocation decision is likely to be the driving force of investment returns in the very long-run but it requires careful maintenance. Managing a pension scheme that is inconsistent with its long-term strategic objectives threatens to derail long-term risk/reward expectations and having such implicit (or, in our view, tactical) short-term asset allocation opinions should be avoided. Instead, a simple yet powerful investment policy of systematic rebalancing that engenders discipline to the asset allocation process should be considered, avoiding inertia or deliberate market timing behaviours and the potential shortcomings of both.

Without such a discipline the trustees are likely to jeopardise the long-term strategic asset allocation decision as the scheme gradually drifts away from its model weightings, acquiring different risk and return characteristics and becoming deprived of genuine diversification benefits.

Preserving an appropriate level of diversification is essential for the fulfilment of a portfolio’s investment objectives over the long term. Our periodic table of investment returns conveys this very clearly, with performance rankings (from better to worse) changing every year seemingly at random. It is hardly surprising that investors are simply unable to forecast the inflection points and consistently pick next year’s top performing asset class. The uncertainty and dispersion of returns across a multitude of capital markets is abundantly apparent, providing overwhelming justification that upholding diversification through rebalancing is a compelling and superior approach.

Rebalancing not only instils a solid diversification discipline but has the potential to influence returns under certain market conditions. In a mean-reverting environment, selling overvalued assets and rebalancing towards those that are undervalued may enhance returns by acting like a ratchet mechanism, compounding a series of incremental benefits over time. However, rebalancing can also cause opportunity loss in long trending environments, testing resolve as it implies continually selling the strongly performing asset and rebalancing to the laggard. Of course, it is unclear in advance whether markets will revert to the mean over the short-term, continue to trend or act completely at random.

Markets are inherently unpredictable and understanding human investment behaviour is a complex field. Fortunately, mechanistic rebalancing offers a readily accessible and useful approach in controlling cognitive biases relating to greed and fear that affect us all, providing reassurance to switch assets when it might otherwise feel emotionally counterintuitive or uncertain to do so.

Rebalancing in Practice

The potential to drift from the strategic allocation will be higher when asset movements are less correlated and, as we have seen recently, when volatility is elevated. Similarly, a longer time horizon will increase the likelihood of deviance and the need to rebalance over time.

In practice, therefore, the chosen periodic and/or range rebalancing approach should be applied in a disciplined fashion having first determined its boundaries and regularity by identifying the tolerance to manage both risk and cost. Overly frequent rebalancing with narrow ranges can be impractical and lead to impairment of investment returns due to the costs of transacting the underlying assets. How far to rebalance can end up being somewhat subjective, partly depending on the extent of any asset weightings not in breach. However, one should bear in mind that trading all the way back to the strategic weight attracts larger transaction costs while trading only to the boundary edge typically incurs more frequent, smaller transactions.

In summary, the strategic asset allocation decision holds such critical importance that it warrants special attention to minimise inadvertent drift away from this adopted long-term policy. While a mechanistic rebalancing strategy may, for better or worse, influence returns over the short-term according to prevailing market conditions, its main premise is to instil a robust risk control and diversification discipline. On balance, we believe the implementation of a well-considered and clearly defined rebalancing policy for all long term investors is an effective way to retain a course that reflects their strategic investment objectives and risk appetite during these most inauspicious or, perhaps, promising times.

|