In the latest inflation update of the Pensions and Lifetime Savings Association’s Retirement Living Standards, people on the Minimum lifestyle have seen the biggest percentage increase to the cost of their retirement, owing to the higher proportion of their budget going towards the things that have risen the most in price: food and energy.

Based on independent research by the Centre for Research in Social Policy at Loughborough University, the Retirement Living Standards describe the cost of three different baskets of goods and services, established by what the public considers realistic and relevant expectations for retirement living. These baskets comprise six categories: household bills, food and drink, transport, holidays and leisure, clothing and social and cultural participation.

Changes to the Retirement Living Standards over the past year and required pot sizes

The Retirement Living Standards are regularly reviewed to ensure they keep up with changes in the public’s expectations of what retired households need as well as the changes to prices on the shelves to remain relevant to real world retirement spending.

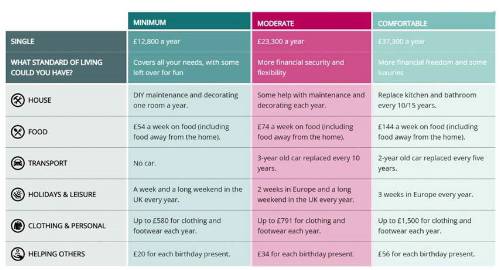

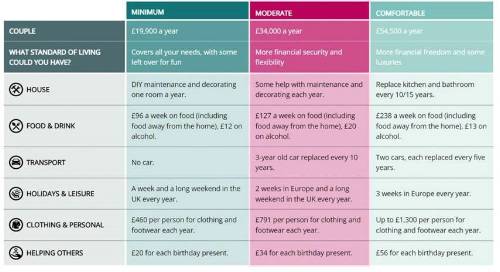

The cost of a Minimum lifestyle increased from £10,900 to £12,800 – or 18% – for a single person and from £16,700 to £19,900 – or 19% – for a couple. The Minimum Retirement Living Standard is the same as the Joseph Rowntree Foundation’s Minimum Income Standard (MIS) and reflects what members of the public think is required to cover a retiree’s needs, not just to survive but to live with dignity – including social and cultural participation. It includes £96 for a couple’s weekly food shop, a week’s holiday in the UK, eating out about once a month and some affordable leisure activities about twice a week. It does not include budget to run a car.

Rising food and fuel prices contributed significantly to the increase in the Minimum standard. The update also saw the amount of food included within the budget increasing to bring it into line with the up-to-date nutritional research on a healthy diet.

The disproportionate increase in the cost of retirement for those on the Minimum Retirement Living Standard means the government’s commitment to the state pension triple lock, announced in the most recent Autumn Statement, is especially important. Rising by a record 10.1% to £10,600 per year, a couple who are each in receipt of a full new state pension would reach the Minimum Retirement Living Standard.

This level should also be very achievable for a single person if they supplement the state pension with income from a workplace pension saved through automatic enrolment during their working life.

The Moderate level increased 12% to £23,300 for a single retiree and by 11% to £34,000 for a couple. The Moderate Retirement Living Standard, in addition to the minimum lifestyle, provides more financial security and more flexibility. For example, a couple could spend £127 on the weekly food shop, have a two-week holiday in Europe and eat out a few times a month.

To achieve this level, a couple sharing costs with each in receipt of the full new state pension would need to accumulate a retirement pot of £121,000 each, based on an annuity rate of £6,200 per £100,000.

At the Comfortable Retirement Living Standard, retirees can expect to have more luxuries like regular beauty treatments, theatre trips and three weeks holiday in Europe a year. A couple could spend £238 per week on food shopping. At this level, the cost of living increased 11% to £37,300 for one person and 10% to £54,500 for a two-person household.

To achieve this level, a couple sharing costs with each in receipt of the full new state pension would need to accumulate a retirement pot of £328,000 each, based on an annuity rate of £6,200 per £100,000.

Automatic enrolment reform needed

Nigel Peaple, Director Policy & Advocacy, PLSA, said: “The past year has been an enormously challenging one for many households in the UK. Inflation has risen to its highest rate in 40 years with the cost of essentials and domestic fuel soaring, putting substantial pressure on incomes for working age and retired households, particularly for those on low incomes. These figures underline why the Government was right to increase the State Pension in line with the Triple Lock in the Autumn Statement.

“The jump in the Retirement Living Standards underscores the need for the Government to adopt the PLSA’s recommendations on pensions set down in our recent report, “Five Steps to Better Pensions”. These include the need for the Government to adopt clear national objectives for retirement income, to ensure the state pension protects everyone from poverty and, later this decade once the cost-of-living crisis has passed, to increase the scope and level of automatic enrolment pension contributions.”

Rising prices affect some goods and services more than others

The annual increase in what is needed to reach each living standard level over the last year is by far the largest since the Retirement Living Standards (RLS) were first established in 2019. Across all of the RLS, the increase in the price of domestic fuel has been the most significant factor in increasing what is needed overall. Between 2021 and 2022, the weekly cost of domestic fuel rose by around 130%. The increase in the weekly cost of domestic fuel accounts for between 30-40% of the increases in the overall budgets for a minimum, moderate and comfortable living standard in retirement between 2021 and 2022.

Increases in the costs associated with motoring at the moderate and comfortable RLS over the past year – driven by increases in the cost of second-hand cars and in the cost of petrol/diesel – have resulted in this element of the budgets increasing by 16%.

At all levels, higher interest rates will help to alleviate the cost pressure of higher prices as savers are able to get more attractive rates on annuities for their retirement pots than in recent years.

• Expenditure on food and fuel are categories that have seen significant price rises over the year and account for around a third of the budget at a minimum, compared to around a quarter at the moderate and comfortable levels.

• The absence of being able to socialise during COVID lockdowns has reinforced for many the need to be able to devote some budget to social activities as a way of participating in society. All budgets include some expenditure on social and cultural participation, accounting for a fifth of the minimum income standard budget but a larger proportion of the moderate and comfortable levels.

• The minimum standard relies on the use of public transport, but at the moderate and comfortable levels car ownership takes up around 10% of the expenditure. Motoring costs have risen significantly driven by increases in the cost of purchasing second-hand cars and by the increases in the cost of petrol/diesel.

|