|

|

The assumptions trustees and sponsors of defined benefit (DB) pension schemes make about asset returns are crucial. Overly conservative assumptions may result in higher contributions that unnecessarily burden pension scheme sponsors, while overly optimistic assumptions could lead to contribution reductions that risk of the security of scheme benefits for members.In recent years, the importance of setting equity return assumptions has diminished somewhat. |

By Mark Tinsley, Principal and Senior Consulting Actuary at Barnett Waddingham Many schemes have reduced their allocation to growth assets and funding levels have generally improved to the extent that fewer sponsors are paying regular deficit reducing contributions. However, this topic remains critical for certain schemes, including many open schemes which tend to hold a significant proportion of their assets in equities and where sponsors are still likely to be paying ongoing contributions. Furthermore, following the recent Government announcement that some of the existing barriers to surpluses being returned to sponsors will be removed, we may be about to see an uptick in the number of schemes that are once again taking an interest in investing for growth. For such schemes, the expected return on equities may be a key factor for trustees and sponsors in deciding whether to continue to run the scheme on. This article explores two popular approaches for setting equity return assumptions:

The Capital Asset Pricing Model (CAPM) approach, which in a UK DB pensions context is usually referred to as the ‘gilts plus’ approach; and In particular, we will illustrate how these two approaches can produce quite different assumptions and discuss what this means for DB pension schemes.

’Gilts plus’ approach

Risk-free rate: This is the theoretical return you'd get if you invested in a completely risk-free asset. While such an asset does not exist in practice, government bonds (gilts) are usually considered to be very low risk investments. Therefore, actuaries often use gilt yields as a proxy for the theoretical risk-free rate. The gilts plus approach then combines the two considerations above to come up with a return assumption. So, if using gilt yields as a proxy for the risk-free rate, an assumption for the return on equities can be determined as follows:

Expected return on equities = Expected return on gilts + An equity risk premium The key advantage of the gilts plus approach is that it is simple to understand and implement. It also has a grounding in observable market data and it arguably aligns with the regulatory framework, noting that The Pensions Regulator (TPR) has previously stated that it benchmarks assumptions against gilts. However, detractors of the gilts plus approach note that it relies on three key assumptions:

that past relationships between gilt yields and equity returns will continue; There is also a question as to whether the return on gilts is indeed the best starting point for determining the risk-free rate. This has been highlighted more so in recent months given the widening gap between gilt yields and swap yields (with 20-year gilt yields almost 1.0% p.a. above swap yields at the time of writing).

Discounted Dividend Model

Expected return on equities = Dividend yield + Dividend growth rate However, the DDM suffers from using backward-looking dividend yields and requiring estimates of future dividend growth, which can be highly uncertain.

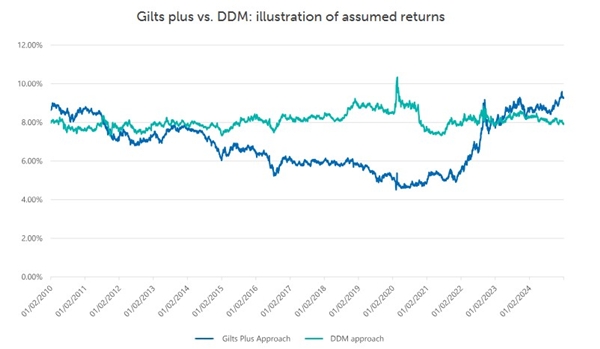

Comparing the two approaches over time

(Assumptions for chart: Gilts plus approach assumption determined as 20-year gilt yield plus 4% p.a.; DDM assumption determined as FTSE Net Dividend Yield plus 20-year gilt implied RPI inflation plus 1% p.a.) The chart illustrates that over the past 15 years, the two methods have produced very different equity return assumptions. For the majority of the 2010s, the discounted dividend model typically provided higher return assumptions compared to the gilts plus approach, following a fall in gilt yields over the decade. So, during this period, adopting the gilts plus approach was likely to lead to higher liabilities and deficit values. However, this is no longer the case. Indeed, following the significant rise in gilt yields in recent years, the chart illustrates that a gilts plus approach may now well yield a materially higher investment return assumption.

Can we expect a shift in regulatory messaging? To be fair to the regulator, it has clarified its stance on several occasions that it is not a 'gilts plus' regulator. Indeed, the new funding code highlights the alternative of the dynamic discount rate approach and there is nothing in regulatory statements that says that the 'plus' part of gilts plus needs to be a constant. Nonetheless, the fact that the regulator does openly use gilts as starting benchmark for assessing valuations, means this perception may be hard to shift. Yet, given the recent divergence of the two models, it is interesting to wonder whether a change in regulatory messaging may be on the horizon. Indeed, as discussed above, the gilts plus approach may no longer be the more prudent option when it comes to member security. Given this, how far-fetched would it be for the 2012 message to be flipped on its head in the upcoming 2025 statement? (Imagine this: “It is the regulator’s view that it would not be prudent to try to second guess market movements by assuming that expectations for equity returns have inevitably improved. Such assessments may turn out to be inaccurate and conceal important risks to the scheme’s ability to meet its liabilities.”) With strong funding positions and low growth allocations, it seems unlikely that we will see anything quite so strong. However, schemes that are relying on (historically) high levels of equity risk premiums may well want to pause for thought and brace themselves for greater regulatory scrutiny.

Embracing uncertainty: a way forward for trustees and sponsors However, this is also the wrong question to ask! There is no such thing as the 'right' model. As discussed, both the gilts plus and DDM methods are underpinned by some sound economic principles, yet they also both have significant flaws. So, a better way forward is to acknowledge that when financial forecasting models diverge it is often a sign of increased uncertainty. In turn, this should be a signal to pause and constructively challenge existing strategies. With this in mind, we suggest trustees and sponsors consider the following actions: Understand differences in views: The recent divergence in the gilts plus and DDM approaches make it much more likely for two different advisers to have two quite different views. While cognitive diversity is a good thing, it is important to understand how these differences of opinion has arisen. For example, do you know if your scheme actuary and investment adviser are using consistent assumptions? If they are not, does this risk a disjointed approach to funding and investment decisions? Re-evaluate and challenge: The temptation to uncritically continue with the same approach used in the past should be avoided. So be prepared to question the assumptions and proposals being put forward by your advisers, especially where a ‘handle turning’ approach is being advocated. Are you comfortable that they have considered alternatives and do they have a robust rationale for using the same approach in a very different set of market conditions? Prepare for different eventualities: The only thing actuaries can be certain of is that a chosen set of assumptions will be wrong. This is true even when different modelling approaches do not significantly diverge. So make contingency plans: if returns are lower or higher than assumed, what actions are you going to take? And how quickly can you take them? The answers to these questions should inform any initial agreement. |

|

|

|

| Head of Capital | ||

| London - Negotiable | ||

| Portfolio Actuary | ||

| London - £140,000 Per Annum | ||

| Deputy Head of Capital | ||

| London - £140,000 Per Annum | ||

| Senior Pricing & Portfolio Management... | ||

| London - £150,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Lead Capital Actuary | ||

| London - £150,000 Per Annum | ||

| Take the lead on capital oversight | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Be at the forefront of creative GI co... | ||

| London/hybrid 2-3dpw office-based - Negotiable | ||

| Remote Market and Credit Risk Calibra... | ||

| Remote - Negotiable | ||

| Contact us about a Capital Contract i... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Head of Insurance Risk | ||

| London - £160,000 Per Annum | ||

| Director - Pensions Risk Transfer (PRT) | ||

| London, Midlands, North West - hybrid working 2dpw in the office - Negotiable | ||

| Dip a toe into public sector work wit... | ||

| Flex / hybrid 2 days p/w office-based - Negotiable | ||

| P&C Consultant | ||

| London / hybrid 3dpw office-based - Negotiable | ||

| Take the lead client-facing projects ... | ||

| Various locations - Negotiable | ||

| Choose Life! Choose a major global co... | ||

| Various locations - Negotiable | ||

| Actuarial skillset? Apply now for Snr... | ||

| South East / hybrid with travel requirements - Negotiable | ||

| Financial Risk Leader - ALM Oversight | ||

| Flex / hybrid - Negotiable | ||

| Be the very model of a modern Capital... | ||

| London - Negotiable | ||

| Pensions Actuary seeking a high-impac... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd