While pensions are not likely to be top of many young people’s priority list, particularly given the challenges of rising living costs, new analysis from Standard Life, part of Phoenix Group, highlights the trade-offs when it comes to balancing near and longer-term financial priorities.

The longer you wait to start contributing to your pensions the more you could miss out on in future

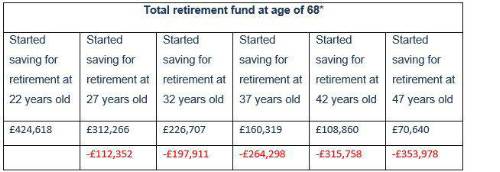

Standard Life’s analysis finds that those who begin working on a salary of £23,000 per year and pay the standard monthly auto-enrolment contributions (3% employee, 5% employer) from the age of 22, would have a total retirement fund of £424,618 by the age of 68. However, waiting just five years to start contributing to a pension, beginning payments at the age of 27, would result in a total pot of £312,266 – over £112,000 less. Waiting even longer could have an even bigger impact on a retirement pot:

*if beginning working with a salary of £23,000 per year and paying 3% monthly contributions into a workplace pension at the age of 22 and assuming 3% salary growth per year

The key difference is that those paying into their pension only later in life will miss out on years of compound interest - when the interest earned on a balance in a savings or investing account is reinvested, ultimately earning more interest. By starting a pension earlier in life and leaving it to grow, compound interest will build each year, meaning those who start saving later on will generally not benefit to the same extent. Of course, putting money away today means there is less of it to meet near term costs, but these figures are intended to highlight the challenge that delaying saving for a number of years can create in the long-run.

Jenny Holt, Managing Director for Customer Savings and Investments at Standard Life said: “It’s amazing to see how just a five-year delay in saving in your 20s can significantly reduce the pension you retire on by tens of thousands of pounds. While times are tough right now with the cost of living continuing to climb, it can be tempting to put off thinking about your long-term financial future and focus purely on the short term.

“However, as our analysis shows, if your finances permit and it’s appropriate for your circumstances, the sooner you engage with and begin to contribute to your pension, the better your ultimate retirement outcome will be. Our calculations show that contributing to your pension from as early an age as possible means the impact of compound interest is much more significant and can result in a much larger retirement pot. For those in a position to do so, consistently paying into a pension from as early an age as possible and topping up payments, especially in your 20s, 30s or early 40s, can make a massive difference over time. The longer you wait to start the worse off you could be by the time you stop working, so if you’re able to save into a pension your future self is likely to thank you for it.”

Standard Life offers tips to maximise pensions savings:

1. Make sure you’re taking advantage of all the benefits of your pension plan and your employer offers. If your employer offers a matching scheme, where if you pay additional contributions your employer will match them, consider paying in the maximum amount your employer will match to get the most out of it.

2. Getting a bonus this year? Deciding to pay some or all of your bonus into your pension plan could save you paying some big tax and national insurance deductions. Meaning you could keep more of it in the long run, and it could be a great way to give your pension savings a boost.

3. Even a small amount could make a big difference in the long term, especially if you’re starting young. If you’re able to, think about paying a little more into your pension when you get a pay rise or have a little extra savings.

|