-

12 million will be eligible to buy State Pension top ups from April

-

Most retiring in the next year will do so with pension pots of £30,000 or less

-

For basic rate tax payers in good health with pots of this size, buying additional state pension could represent better value than buying an annuity

-

As with pensioner bonds, take-up could be much higher than the government expects, costing the Treasury more than the £415m it anticipates in the next financial year, going up to £435m the following

-

Urgent need for better guidance to help individuals find best retirement solutions for them

Chris Noon, Partner at Hymans Robertson, explains:

“Most people retiring with DC pensions in the next few years will be doing so with pension pots of less than £30,000. The new flexibilities from April will allow these individuals to take that money out and do what they want with it. While many will simply take this as cash, some may want to use it to buy a regular income to last the remainder of their life.

“There is an interesting, but not widely known, consequence of the retirement revolution. Those who’ve already retired or who are due to before April 2016, and who want a lifelong regular income, will be able to take money out of their DC pots and use this to buy more State Pension.

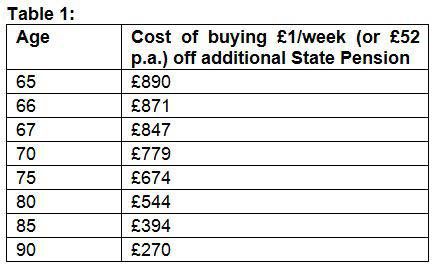

“Everyone retiring before 2016 will be able to buy an additional £1 of state pension for roughly £890. This top up will be inflation-linked, included a survivor’s pension and have a ceiling of approximately £25 per week. This will cost up to £25,000.

“Given this route will be much better value than annuities for some, there could be parallels to Government’s pensioner bond scheme, where demand is far greater than the government anticipates. It estimates take-up in the region of 265,000, with a cost to the Treasury of £415m for the next financial year. The financial impact on government coffers could be much greater.

“There will be value in doing this for some, but not all retirees. It won’t be as attractive an option to those who have had episodes of ill health or who are higher rate tax payers. But it could be better value for those with smaller pots, with no health problems and who pay the basic rate of tax. It will be even better value for those who are older as the costs decrease with age (see table 1 below).”

Commenting on the challenges presented by the new pension freedoms, he added:

“The new flexibilities mean a proliferation of options for retirees. With choice comes complexity. There needs to be more support given to those retiring from April to allow them to make the best of their new found freedom.

“The focus thus far has been on helping people at the point of retirement with initiatives such as the Guidance Guarantee – which arguably doesn’t go far enough. However, we need to also turn our attention to those from age 55+ that haven’t retired but who may start drawing on their pension funds, as well as those in retirement who begin eating through savings without help from an adviser.

“While the need for more support for individuals is indisputable, this usually comes at a cost. Those with small pots are unlikely to be in a position to pay for that support. As such, the need for low cost online tools that guide individuals towards the optimal options for them, and to have such tools in place from at least 10 years before retirement, could not be greater.”

Chris Noon gives an example of how the State Pension tops ups could work:

“Assume an individual reaches State Pension Age in October 2015. They are entitled to a State Pension of £7,000 and have a DC pot of £20,000. They need a regular annuity income from the DC pot. The £20,000 could buy an inflation-linked annuity of around £600 (including a spouse’s pension). Alternatively, taking the £20,000 as cash would provide £17,000 after tax. Using this £17,000 to buy additional State Pension would provide additional annual income of £1,050. In this example, that’s 75% more than the annuity could provide. It’s worth caveating that annuities do make sense for some and an individual needs to consider their own specific circumstances.”

|