The Broadstone Sirius Index – a monitor of how various pension scheme strategies are performing on their journeys to self-sufficiency – posts its latest update.

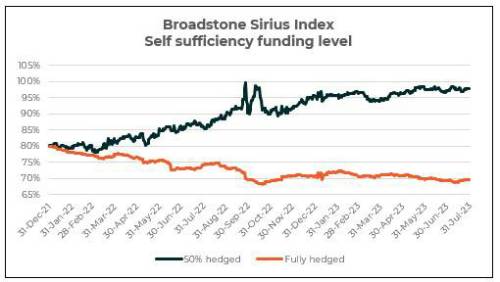

The July update of the Broadstone Sirius Index found that fully hedged schemes continued to provide low volatility in funding, with its funding position remaining steady at 69.6% through to the end of the month.

Funding has improved slightly through the month (69.5% in June) but slightly fallen from its position at the end of 2022 (70.8%).

The 50% hedged scheme made a small gain with a 0.7 percentage point funding level improvement, maintaining its strong funding position at 97.8%. This marks a small uptick in funding level from 95.4% at the end of 2022.

David Brooks, Head of Policy at Broadstone, commented: "Pension funding conversations with Trustees and sponsors are not meant to be exciting and our experience over the last few months has shown that things are calming down.

“All those involved with defined benefit (DB) schemes want to see small positive improvements but without great leaps either way. Movement in the extremes up or down suggest risk which is something we want to remove from DB funding conversations.

“The rhetoric from government to find ways to increase risk in DB pension schemes, should be understood in the context that not all schemes are fully funded on a buy-out basis. Funding has improved, but for many schemes there is some way to go until their members’ benefits are secure.

“Employers are still on the hook for millions of pounds in buy-out deficits and understanding and controlling the risks they’re exposed remains paramount. Let’s not forget our funding basis is focused on low dependency which means both our schemes will have significant buy-out deficits that still need to be filled.

“The government’s desire to increase risk may be misstep as the schemes that can buy-out will and the ones that can’t continue their slow and steady journey.”

|