-

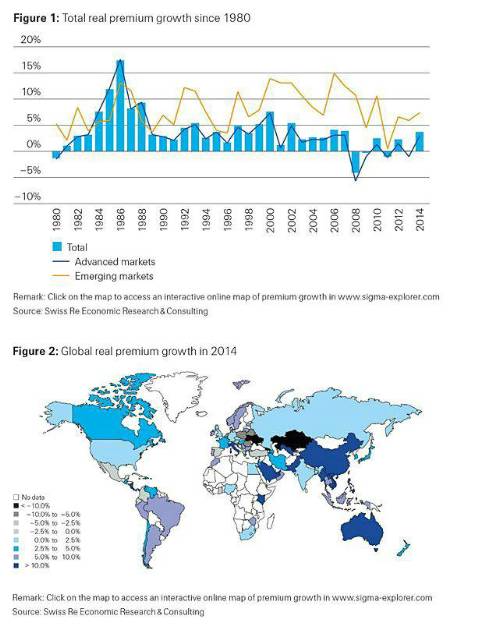

Global life premiums returned to positive real growth of 4.3% in 2014, above the pre-financial crisis average

-

Non-life premiums were up 2.9% in 2014, based largely on continuing improvement in the advanced markets

-

Profitability in life improved slightly last year, but underwriting results in non-life, though positive, were slightly weaker

-

Life premiums to grow further in both the advanced and emerging markets in 2015; non-life premium growth will be strong in the emerging, but sluggish in the advanced markets

Advanced markets boost growth in life premiums

In the life sector, there were considerable variations in the premium growth outcomes across different regions. For instance, very strong growth in Oceania, and solid results in Western Europe and Japan more than offset yet another year of contraction in North America. In the emerging markets, life premiums grew by 6.9% compared to 3.6% in 2013. The rise was driven mainly by China, where new distribution channels such as online sales and a recovery in bancassurance boosted premium income. In other emerging regions, however, premium growth generally slowed or even declined.

Life premiums in the advanced markets grew by 3.8% in 2014, continuing a volatile pattern of growth and contractions since 2010. "Despite the acceleration in 2014, overall advanced-market life insurance premiums are about the same level as before the steep drop in volumes in 2008," says Kurt Karl, Chief Economist at Swiss Re. "The gain in premiums in 2014 outpaced economic growth, increasing insurance penetration in the advanced markets, but premiums post-crisis have been growing at a much slower rate than before the financial crisis."

Stronger performance in advanced markets boosts non-life also

Non-life premium growth has been gradually improving since 2009, but still averages less than in the pre-crisis years. In non-life too, the gain in global premiums in 2014 was driven by a substantially stronger performance in the advanced markets. In North America, premiums were up 2.6% from the previous year and in Western Europe premiums returned to positive growth (+0.6%) after years of decline and sluggishness.

This sigma includes a special chapter on the stagnation of non-life premiums in Western Europe since 2007. Private medical insurance premiums have been the bright spot, continuing to grow robustly throughout Europe. But premium growth in the southern peripheral countries in particular has been very weak since the financial crisis and, by line of business, casualty (especially motor) has contracted sharply. However, " the past seven years should not be seen as a benchmark for upcoming growth performance in the European non-life markets. The economic environment, though still weak, is likely to continue to improve, and when unemployment falls, non-life premiums, including motor, will recover," notes Daniel Staib, co-author of the report.

In the emerging markets, non-life premiums grew by a robust 8.0% in 2014. The key drivers were solid gains in China, mainly in the motor, credit & guarantee and agricultural lines, and in India where an improvement in business sentiment and economic growth boosted premiums. In both the advanced and emerging markets, the post-crisis annual average premium growth rate has fallen short of the pre-crisis pace.

Low interest rates to continue to affect profitability

Overall profitability in the life insurance sector improved slightly in 2014, driven by stronger stock markets, higher premium growth and cost containment efforts. Underwriting results in non-life were positive but slightly weaker than in 2013, because claims experience deteriorated slightly and contributions from prior-year reserve releases lessened. Both the life and non-life sectors continued to suffer from low interest rates and overall industry profitability remains below pre-crisis levels.

Life premium growth is expected to remain fairly solid in the advanced regions in 2015 and increase in the emerging markets, particularly in Central and Eastern Europe and China. The US life market is likely to improve alongside the strengthening economy and jobs market but in Western Europe, premium growth will slow from the strong gain in 2014. The outlook for the non-life industry in advanced markets is more moderate. Premium rates remain low and though economic growth is improving, it remains sluggish. Non-life premium growth in the emerging markets, on the other hand, is expected to remain robust.

Irrespective of positive premium developments, once again overall industry profitability is expected to fall short of pre-crisis levels in 2015. Investment yields – a key component of profitability in the life sector – will remain under pressure from the low interest rate environment. Life insurers' profitability is unlikely to improve markedly any time soon, given that the burden from low yields and ongoing regulatory changes will continue. The same is true in non-life, where weaker underwriting results – due to flat or even lower rates and a smaller contribution from reserves releases – will also weigh on earnings.

|