Climate change and digitalisation are significant trends shaping the world economy and insurance markets. Rapid decarbonisation is becoming imperative and societies' approach to transitioning to a green economy will determine the economic outlook. The insurance industry can support the transition to a low-carbon economy, not only by absorbing disaster losses but also by promoting sustainable infrastructure investments that help mitigate the impact of volatile extreme weather. Adopting digital technologies is not only playing a role in increasing global productivity growth, but Swiss Re research also found that the pandemic has transformed consumers' receptiveness to interacting with insurance digitally, pointing to growth potential.[1] A third significant trend is the growing divergence of countries' growth and socio-economic indicators such as inequality – a potential downside risk.

“The economic recovery we are experiencing is cyclical and not structural, with macroeconomic resilience weaker today than before the COVID-19 crisis. As such, we should be anything but complacent. Given its capacity and expertise to absorb risks, the insurance industry is crucial in making societies and economies more resilient. Yet for inclusive and sustainable growth, everyone must be on board. Green growth is sustainable only if it is also inclusive. We have a unique opportunity to build a better market system. For this, all stakeholders will need to accept and internalise the costs of climate change, and policymakers to take into account the distributional effects of their economic policies across their populations. This will help to create the transition we need for a sustainable path to a net-zero economy by 2050," said Jerome Haegeli, Swiss Re Group Chief Economist.

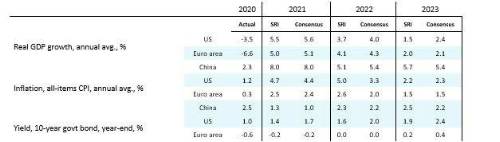

Swiss Re Institute's sigma study forecasts that global GDP growth will be strong in 2021, at 5.6%, slowing to 4.1% in 2022 and 3.0% in 2023. Inflation is the prevailing near-term macro risk, fuelled by the energy crisis and prolonged supply-side issues. The price pressure is expected to be most acute among emerging markets and in the UK and US.

Market rebound reflects resilience of insurance industry

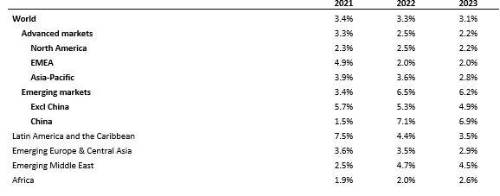

Swiss Re Institute estimates that global non-life premiums will grow by 3.3% in 2021, 3.7% in 2022 and 3.3% in 2023. Property-catastrophe rates are forecast to improve in 2022 after a year of above-average losses. Casualty rates should also be stronger next year due to ongoing social inflation while personal lines are expected to benefit from early signs of improving motor pricing in the US and Europe. Global health and medical insurance premium is expected to rise, driven by growth in the US economy and stable advanced market demand. Expansion in emerging markets is expected to be strong, with China projected to grow by 10% in each of the next two years, largely driven by strong demand for medical insurance, including critical illness covers.

Global life premiums are expected to increase by 3.5% in 2021, 2.9% in 2022 and 2.7% in 2023. Protection-type products should see strong demand, supported by higher risk awareness, a recovery in group business and increased digital interaction. Savings business is expected to grow moderately in the next two years, reflecting a slight improvement in government bond yields and a recovery in employment and household incomes. As the pandemic continues to affect the life insurance industry, excess mortality shows a mixed trend. Unlike many European countries, the US has experienced continuous excess mortality since the start of the pandemic and death benefits paid increased in the first half of this year. Life insurers in Latin America have faced unprecedented pandemic claims as the region has been hit particularly hard by COVID-19. In Brazil, the life insurance benefit ratio more than doubled in April 2021, while the pandemic is the costliest event ever recorded for the local insurance industry in Mexico, totalling USD 2.5 billion in insured losses over 18 months as of September 2021. This surpasses the USD 2.4 billion loss from hurricane Wilma in 2005.

Rising risk awareness is generating demand for more insurance protection. The pandemic shock has highlighted the important role the insurance industry plays as a risk absorber in times of crisis by providing financial relief to households, businesses and governments. At the same time, supply chain disruptions show that better protection is required to improve societal resilience and record-breaking weather extremes this year add urgency to the global race to net zero. Consumers also welcome digital and online insurance, and it is expected to grow rapidly. However, increasing inequality could exacerbate social inflation, which is defined as the increase in insurance claims driven by large litigation costs.

"Market conditions suggest that positive pricing momentum will continue across all lines and regions. Inflation-driven higher claims development in all lines of business, continued social inflation in the US and persistently low interest rates will be the main factors for market hardening," said Jerome Haegeli.

Table 1: Real GDP growth, inflation and interest rates in select regions, 2020 to 2023

Note: Euro area policy rate refers to the interest rate on the main refinancing operations; data as of 11 November 2021. Source: Bloomberg, Swiss Re Institute.

Table 2: Total insurance premium growth forecasts, in real terms

Source: Swiss Re Institute.

|