|

|

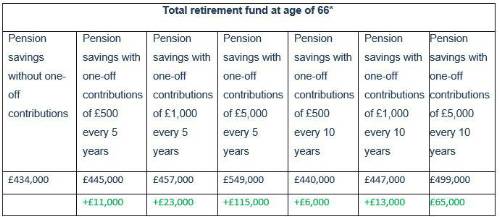

One-off pension contributions of £1,000 every 5 years could boost your pension by £23,000 in retirement. This Pension Engagement Season, Standard Life calculations highlight the benefits of topping up your pension savings with one-off contributions throughout the course of your career |

People might not think of their pension when they get a generous birthday gift or a bonus, however new analysis from Standard Life, part of Phoenix Group to coincide with this year’s Pension Engagement Season reveals that those who boost their pension savings with one-off contributions every few years could generate thousands more in retirement savings. Making ad-hoc payments into a pension throughout someone’s working life can go a long way towards building a healthy pot in retirement. Even smaller contributions can end up making a noticeable difference after they’ve had the chance to grow and benefit from compound investment growth. Standard Life’s analysis finds that those who begin working on a salary of £25,000 per year and pay the minimum monthly auto-enrolment contributions (3% employee, 5% employer) from the age of 22, could have a total retirement fund of £434,000 by the age of 66, not adjusted for inflation. However, those who topped their pensions up with nine one-off payments of £500 every 5 years, from the age of 25 to 65, could find themselves £11,000 better off in retirement. Of course, those in a position to contribute more have the potential to amass a larger retirement fund – for example paying in £5,000 every 5 years, between the ages of 25 to 65, could result in a total pot of £549,000 – £115,000 more than if no additional contributions had been made. One-off contributions and retirement fund

It’s always a trade-off as putting money away means there’s less of it to meet short-term costs or luxuries now, but these figures highlight the potential potency for one-off contributions to build up over a long period of time, particularly when possibly benefiting from the power of compounding. |

|

|

|

| Reinsurance Pricing Actuary | ||

| London - £140,000 Per Annum | ||

| Head of Capital | ||

| London - £170,000 Per Annum | ||

| ART Pricing | ||

| London - £100,000 Per Annum | ||

| Pricing Transformation Actuary | ||

| London - £130,000 Per Annum | ||

| Pricing Actuary | ||

| London - £80,000 to £120,000 Per Annum | ||

| Pensions on Divorce Startup - Flexibl... | ||

| Remote - Negotiable | ||

| SVP, Head of Reserve Forecast Analytics | ||

| Bermuda - £200,000 Per Annum | ||

| START-UP, Lead Reinsurance Actuary | ||

| London - Negotiable | ||

| Senior Actuary | ||

| London - Negotiable | ||

| Reserving Manager | ||

| London - £130,000 Per Annum | ||

| Senior Reserving Consultant | ||

| London - £100,000 Per Annum | ||

| Head of Capital | ||

| London - £180,000 Per Annum | ||

| Head of Portfolio Optimisation | ||

| London - Negotiable | ||

| Pricing Lead/Manager | ||

| London - £130,000 Per Annum | ||

| Actuary | ||

| London/Hybrid - Negotiable | ||

| Capital Actuary | ||

| London - £110,000 Per Annum | ||

| Senior Reserving Actuary | ||

| London - Negotiable | ||

| Head of Capital | ||

| London/Hybrid - Negotiable | ||

| Head of Pricing | ||

| London - £170,000 Per Annum | ||

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd