|

|

For a while now, we’ve been looking at the impact of the slump in rates of return over the last decade on those who are saving for their retirement. The usual argument is that people need to save more to compensate, hence our paper earlier this year on ‘is 12% the new 8%’. But we’ve now turned our attention to what younger people can do if they can’t afford to save more. As you might expect, the options are to seek higher returns through taking more risk and/or to work for longer. But how much more risk and/or work how much longer? |

We think this is particularly relevant given that most workplace pension default funds are (by design) meant to be broadly OK for most of the membership and therefore may not take enough risk for younger workers in any case. But younger workers may simply not be sufficiently engaged to review how their money is invested. In a previous paper LCP and interactive investor showed how falling investment returns have made saving for a decent retirement an even higher mountain to climb. For example, the previous research found that someone enrolling in a pension today would need to contribute 12% of pay to achieve the same pension as someone contributing 8% a decade ago whose investments grew in line with expectations at the time.

But for some people increasing contributions like this is simply not an option.

If they still want to achieve a decent pension in this tougher environment, today’s new savers have two options besides increasing contributions:

- Work for longer, giving more time to build up a pension pot

- Take more risk, generating a higher expected investment return over the long run for any given level of contributions

New research from LCP has revealed for the first time the dramatic scale of the changes which younger savers would need to make to offset plunging investment returns.

The research asks the following question:

“To offset falling expected investment returns, what would a worker have to do in terms of a) working longer and/or b) taking more investment risk, to end up with the same pension that a similar worker would have expected ten years ago in a world of higher returns than today”.

In effect, this is the ‘running to stand still’ question.

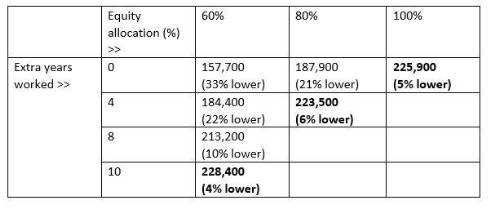

The key baseline figures for the expected pension pot of a new worker with a starting salary of £22,437 per annum (which is about £430 per week before tax) saving 8% of ‘qualifying earnings’ into a pension from age 22 in today’s money are:

With 2007 expected investment returns (and 2% annual real wage growth on top of inflation): pension pot at age 68: £236,800 With 2017 expected investment returns: pension pot at age 68: £157,700 (Note: These figures are based on the assumption that the money is invested in a ‘default fund’ comprising 60% equities and 40% bonds. 2017 is the date of the most recent investment return projections on which current FCA rules are based. Sums are shown in today’s money, so take account of the effect of inflation).

To get more-or-less back to a pot of roughly £236,800, LCP finds that the worker could either: The following table shows the results for different combinations of working longer and taking more risk: Base case: 8% contributions, 2007 era investment returns forecast, balanced portfolio. UK average salary, 2% real wage growth Assets at age 68 = £236,800 [ in today’s money terms] Updating for new 2017-era expected investment returns, varying extra years of work and asset allocation

The table shows:

To broadly offset this decline, options include: Around five in six workers who have been automatically enrolled into a workplace pension will be invested in a ‘default’ fund. But default funds are designed to be broadly suitable for the scheme membership as a whole and may tend to be too cautious for younger investors. Members may not always realise that they can generally change the investment mix and younger members in particular could consider taking more investment risk if appropriate to their circumstances if they want to avoid having to work far longer or contribute far more. Default funds also vary very substantially in terms of their allocation to equities and this is crucial for younger savers. A survey by EY indicates that the asset allocation even of the default fund in popular Master trusts can vary substantially from around 35% in equities (or stocks) to 100%. The difference between these is vast today in terms of future returns, especially for the younger investor. Taking on more investment risk is likely to mean that pension assets could fluctuate by more than usual each year, and the suitability of this strategy will vary from individual to individual. However, much pension language frames options in a particular way and this can lead to an over-focus on risk and not enough focus on returns. But this can lead younger investors down a path of “reckless prudence”. Younger investors may well wish to re-evaluate this trade-off. Research by interactive investor in 2020 amongst people with life company pensions found that 27% of people say they are in a low risk pension. Even amongst the younger generations (18-34 year olds), over a fifth (22%) said they had a low risk pension and over a quarter (26%) of 35-54 year olds.

Commenting, LCP partner Dan Mikulskis said: Taking more investment risk is always a tricky balance, but by moving more of their pension into growth assets such as equities, younger people could expect a better return and could save themselves having to work well into their seventies. At the very least, all investors should be ‘looking under the bonnet’ to find out how their pension fund is being invested and asking the question what the right level of investment risk is for them”. Becky O’Connor, Head of Pensions and Savings at interactive investor, said: “ The thought of having to work until almost 80 years old is enough to fill even the most active and ambitious among us with dread. It should at least be enough to encourage a closer examination of our pension funds to see if they are working hard enough – so we can eventually stop working. Any small changes made now to boost the growth potential of your pension could save years of graft later on.

“Taking more risk with a pension - your life savings - might sound counter intuitive, but actually in today's ‘lower for longer’ growth environment, low interest rates and rising inflation, it is a sensible strategy, provided you are investing for the long term.” |

|

|

|

| Pricing Lead/Manager | ||

| London - £130,000 Per Annum | ||

| Actuary | ||

| London/Hybrid - Negotiable | ||

| Capital Actuary | ||

| London - £110,000 Per Annum | ||

| Senior Reserving Actuary | ||

| London - Negotiable | ||

| Head of Capital | ||

| London/Hybrid - Negotiable | ||

| Head of Pricing | ||

| London - £170,000 Per Annum | ||

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Head of Capital | ||

| London - Negotiable | ||

| Portfolio Actuary | ||

| London - £140,000 Per Annum | ||

| Deputy Head of Capital | ||

| London - £140,000 Per Annum | ||

| Senior Pricing & Portfolio Management... | ||

| London - £150,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Lead Capital Actuary | ||

| London - £150,000 Per Annum | ||

| Take the lead on capital oversight | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Be at the forefront of creative GI co... | ||

| London/hybrid 2-3dpw office-based - Negotiable | ||

| Remote Market and Credit Risk Calibra... | ||

| Remote - Negotiable | ||

| Contact us about a Capital Contract i... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Head of Insurance Risk | ||

| London - £160,000 Per Annum | ||

| Director - Pensions Risk Transfer (PRT) | ||

| London, Midlands, North West - hybrid working 2dpw in the office - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd

Our new research, jointly between LCP and Becky O’Connor at Interactive Investor, find that on unchanged investment and unchanged contributions, you would need to work an extra *10* years to make up for the slump in returns. Or you could switch from a typical 60% equity workplace pension to a 100% equity fund to give the higher (expected) returns you now need. Or a combination – eg 80% equities and work four years more.

Our new research, jointly between LCP and Becky O’Connor at Interactive Investor, find that on unchanged investment and unchanged contributions, you would need to work an extra *10* years to make up for the slump in returns. Or you could switch from a typical 60% equity workplace pension to a 100% equity fund to give the higher (expected) returns you now need. Or a combination – eg 80% equities and work four years more.