|

|

A number of insurance companies have been writing significant volumes of Equity Release Mortgages (“ERM”) and using these as assets to back annuities. Unlike other backing assets, such mortgages are retail customer products themselves, and therefore do not easily conform to the concepts usually applied to assets traded through wholesale markets. |

By Scott Eason, Partner & Head of Insurance Consulting and Michael Henderson an Associate from Barnett Waddingham

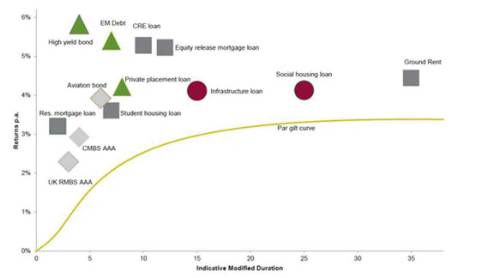

The following graph produced by the IFoA Non-Traditional Assets Working Party shows the attractiveness of Equity Release Mortgages. As well as providing a significant uplift in yield over gilts, the off-setting longevity risk reduces capital requirements for annuity writers.

For many annuity writers, the ability to source ERMs has been a significant competitive advantage and led to it being considered as a “super-asset”.

However, on 6 November 2015, the PRA announced an intention to undertake an insurance industry-wide review of Equity Release Mortgage (“ERM”) valuations and capital treatment during 2016 within its Solvency II Directors’ update.

Separate Box

There are two main types of equity release plan:

With a lifetime mortgage, you take out a loan, secured on your property, and receive that amount as a tax-free lump sum. You do not usually make monthly repayments. Instead, the interest “rolls up”, and the loan plus interest is repaid after your death, when the property is sold. A “No Negative Equity Guarantee” feature is usually provided, meaning that the customer’s estate never has to repay more than the sale proceeds of the property (even if the accumulated loan is greater).

With a reversion plan, you sell all or part of your home in return for a tax-free lump sum and a guaranteed lifetime lease, with no monthly repayments to meet. After your death the house is sold, so the lender gets back its percentage share.

Why is the PRA concerned about ERM?

These are illiquid assets with no liquid secondary market, and so asset valuations are typically marked-to-model and dependent on many assumptions, including future interest rates, individual property price inflation, transitions to care homes and individual longevity, which in many cases are volatile, subjective and un-hedgeable.

The PRA are keen to ensure that companies are complying with Solvency II requirements in areas such as asset valuation and the prudent person principle.

Matching Adjustment (“MA”) securitisation

To be eligible for matching adjustment, assets backing annuities must be “bond-like” and have fixed cash-flows. The uncertainty around the timing and amount of the redemption of the mortgages has been deemed to make them ineligible in their original form.

To make these assets eligible for MA, firms have been securitising their ERMs and creating a senior tranche that does have fixed cashflows and is eligible for a MA portfolio, and an equity tranche that picks up the uncertainty and is held outside of the MA portfolio. The tranching adds to the complexity of valuations and although the underlying risks are unlikely to be materially changed, the overlaying of a structure (and the regulatory requirements which come with it) is likely to add significant complexity and cost to the management of the underlying risks.

Solvency II Marked-to-model valuation requirements

The default valuation method for assets is to use quoted market prices in active markets for those assets. A first alternative is to adjust quoted market prices in active markets for similar assets. Neither of these are possible for the ERM tranches.

Alternative valuation methods are allowed but must use techniques that are consistent with one or more of the following approaches:

The methods need to rely as little as possible on undertaking-specific inputs and make maximum use of relevant market inputs.

A number of different models are being used to value ERMs with most being multi-variable models that aim to predict the impact on property prices, interest rates and longevity under various scenarios, often run stochastically. A large amount of expert judgement is inherent in the assumptions and interactions.

Prudent Person Principle requirements

The PPP requirements are set out in Article 132 of the Solvency II Act. The relevant requirements are:

Additional Solvency II asset requirements

Additional requirements are set out in the Solvency II Act, the Delegated Act and Level 3 guidelines • The Solvency II Act requires written risk management policies on ALM, investments, liquidity and concentration risk. • The Delegated Act set out requirements in respect of assets not valued by market value, requirements in terms of loans, and further detail on the risk management policies • L3 guidelines give even further guidance on the written content, and also require that companies don’t rely on external ratings for determining risk.

What should companies do now?

As you can see from the above, there is a lot of process and documentation that is required to be in place in respect of all assets, and holding mark-to-model assets such as ERM adds to the requirements.

Despite recent reductions in spreads, ERMs remain a super-asset for annuity writers, providing a superior return net of cost of capital compared to more traditional corporate bonds and many alternative credit assets. They also provide some hedge to longevity risk on annuities. Losing the ability to use these assets to back annuities will reduce the competitiveness of many writers and reduce value for individuals or pension schemes purchasing annuities. It may also impact the size of the ERM market, reducing the availability of a product with a clear social need.

We recommend that companies assess now, in advance of the planned PRA review, their policies and documentation in respect of all assets, but particularly ERM, to ensure compliance with the Solvency II requirements. In particular, we believe that the PRA’s review of this asset class as part of the approval of an Internal Model may not necessarily mean that an insurer will not be subject to criticism by the PRA as part of the more detailed and focused ERM review.

By working ahead of the industry review, companies can make the exercise a lot less painful than it could otherwise be and continue to take advantage of the asset class.

|

|

|

|

| Portfolio Actuary | ||

| London - £140,000 Per Annum | ||

| Deputy Head of Capital | ||

| London - £140,000 Per Annum | ||

| Senior Pricing & Portfolio Management... | ||

| London - £150,000 Per Annum | ||

| Pricing Transformation Lead | ||

| London - £85,000 Per Annum | ||

| Lead Capital Actuary | ||

| London - £150,000 Per Annum | ||

| Take the lead on capital oversight | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Be at the forefront of creative GI co... | ||

| London/hybrid 2-3dpw office-based - Negotiable | ||

| Remote Market and Credit Risk Calibra... | ||

| Remote - Negotiable | ||

| Contact us about a Capital Contract i... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Head of Insurance Risk | ||

| London - £160,000 Per Annum | ||

| Director - Pensions Risk Transfer (PRT) | ||

| London, Midlands, North West - hybrid working 2dpw in the office - Negotiable | ||

| Dip a toe into public sector work wit... | ||

| Flex / hybrid 2 days p/w office-based - Negotiable | ||

| P&C Consultant | ||

| London / hybrid 3dpw office-based - Negotiable | ||

| Take the lead client-facing projects ... | ||

| Various locations - Negotiable | ||

| Choose Life! Choose a major global co... | ||

| Various locations - Negotiable | ||

| Actuarial skillset? Apply now for Snr... | ||

| South East / hybrid with travel requirements - Negotiable | ||

| Financial Risk Leader - ALM Oversight | ||

| Flex / hybrid - Negotiable | ||

| Be the very model of a modern Capital... | ||

| London - Negotiable | ||

| Pensions Actuary seeking a high-impac... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Great opportunity for Pensions Actuar... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd