Pausing pension contributions mean savers miss out on thousands in future

Standard Life’s research, based on a survey of over 2,500 customers, shows that if they had to cut down on expenses 15% would put less money into savings accounts, and 6% would reduce their pension contributions.

This low figure is encouraging, as Standard Life analysis2 reveals that reducing or stopping pension contributions, even for a relatively short period of time, can have a significant impact on the final pot – with savers potentially being thousands of pounds less well off in retirement as a result.

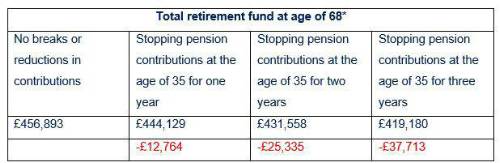

For example, someone that began working with a salary of £25,000 per year and paid the standard monthly auto-enrolment contributions (3% employee, 5% employer) from age of 22, would have a total retirement fund of £456,893 at the age of 68. However, stopping pension contributions at the age of 35 for just one year, would result in a total pot of £444,129 – almost £13,000 less than if they had not stopped paying in. Stopping contributions for a longer period would have an even bigger impact:

Total retirement fund at age of 68*

*if beginning working with a salary of £25,000 per year and paying 3% monthly contributions into a workplace pension at the age of 22

Cost of living bites

While currently relatively low, the risk of consumers sacrificing savings to cover everyday expenses continues as long as these challenging circumstances go on. Over three quarters (77%) expect to have to cut back on spending or saving, and unsurprisingly those with less household income are having to make the most cuts. For households with less than £20k in income, 86% say they’ll need to reduce their spending and saving, with 83% of households with between £20,001 and £30k income saying the same. This compares to less than three quarters (72%) of households with £70,001-£100k income, and 56% of households earning more than £100k.

Almost all (93%) say that increasing costs and high inflation are going to impact, or are already impacting, their financial situation, rising from 88% in Q1 this year. More than four fifths (85%) say higher fuel costs have affected their finances (up from 76% in Q1), while 93% are feeling, or will feel, the effects of higher energy prices on their finances (up from 88% in Q1).

Jenny Holt, Managing Director for Customer Savings and Investments at Standard Life said: “Consumers have had to contend with a lot so far this year, and since April alone we have seen the increase to the energy price cap, higher national insurance contributions, as well as inflation recently reaching 9.1%. This is of course taking its toll on people’s finances, with many having to cut back on spending and saving as a result.

“If possible, the first port of call should be to reduce spending – for example cutting back on unnecessary purchases and shopping around for better value deals. Doing this, rather than making decisions that will affect future finances such as reducing or stopping pension contributions, even if for a short period only, will be beneficial in the long term.”

When it comes to making cutbacks, reassuringly customers are currently doing just this. If they needed to cut down on expenses, half of Standard Life customers would reduce their energy usage (51%) and spend less on luxuries (51%). Three in ten (30%) would eat out less, while 23% would reduce their subscription services and 23% would also go on fewer holidays.

Jenny Holt at Standard Life shares tips for potential spending cutbacks in the current environment:

1. Review your expenditure for potential areas of savings – “By looking through your monthly outgoings, you may find there are ways to make savings. Do you have any subscriptions or memberships that you no longer use and could cancel or pause? Do you spend a lot of money on things that are a luxury, such as takeaways? Taking some of these small steps could make a difference.

2. Shop around for better deals – “You may be able to switch household providers and find cheaper deals – such as for broadband or your mobile phone. Many providers have package deals for new customers so it’s worth using a price comparison website to see if there are savings to be had.

3. Set budgets – “To help you keep an eye on your outgoings, it may be worth setting a budget for things like food shopping and socialising so you don’t spend more than your means.”

|