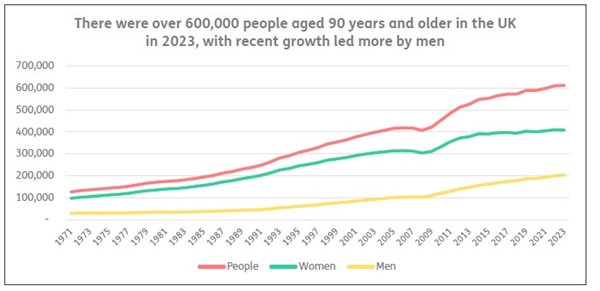

Nearly 612,000 people aged 90 or over are living in the UK with the number heading upwards, according to official figures1 that underscore the need for those heading into retirement to be realistic about how long they will need their pension income to last. Figures for 2023 from the Office for National Statistics show the number of people aged 90+ has doubled over the last 30 years and only dropped marginally during the coronavirus pandemic followed by two years of strong rises. The number of centenarians has doubled in 20 years to more than 16,000. The ratio of women over age 90 to men was about 2:1 in 2023 compared to 4:1 in the 1980s. About one in every 100 people is now aged at least 90.

Stephen Lowe, group communications director at retirement specialist Just Group, said that the figures show that people heading into retirement need to take account of the significant possibility of living to age 90 and beyond. “It’s very tricky to apply life expectancy figures to retirement planning because individuals are very unlikely to be average – none of us know if we will be hit by the proverbial bus tomorrow or live to get a card from the King.

“However, official figures do show the odds of living to beyond 90 are high enough that people shouldn’t assume it can’t happen to them. Historically, this has been mainly women but the numbers of men are catching up fast. For those who are 66 this year and starting to take State Pension, there is about a one in three chance (33%) for men and nearly an evens chance (46%) for women of making it to at least age 90. And if they do get to age 90 there is nearly an evens chance they will survive beyond 95.”

He said that planning for retirement involves covering all the ‘what ifs’ of later life. “There are really three scenarios to consider – you die around average life expectancy, or you die sooner, or you live longer. The plan needs to cover all three bases.”

An annuity is the only financial solution people can choose that is guaranteed to keep paying an income for however long someone lives. He said that these are often mispresented as a ‘bet on how long you live’ with the unlucky ones who die early losing out. “In reality, most annuity buyers opt for a guaranteed period that can pay income to a beneficiary for a set time after death, or capital protection that pays out a lump sum from the money used to buy the annuity less any income already paid out, or a spouse’s pension that keeps paying for a partner’s lifetime. If you select the right options, the money spent on buying an annuity will always be returned.

Sales of annuities have been increasing recently due to a rise in rates that makes them more attractive relative to other options that are more flexible but don’t provide income guarantees.

“Many retirees enjoy the peace of mind of having a regular flow of secure income that is sufficient to know their daily outgoings are covered,” said Stephen Lowe. “That can come from State Pension, defined benefit pensions or annuities. Once the basics are covered, other money can be spent, invested or gifted. The important thing for those considering annuities is to choose the right options and to shop around for the best deal. A little extra at the start can add up to thousands of pounds over a long retirement.”

Annuity buying tips:

• MoneyHelper – www.moneyhelper.org.uk – the government’s money and pensions guidance service offers access to free, independent and impartial guidance service Pension Wise and also has a useful online tool allowing quick comparisons of annuity rates and options.

• Employ an expert – an annuity broker or regulated adviser will work with you to better understand your goals, to choose the right options and shop around for the best deal.

• Full disclosure – providing details of your lifestyle and medical history is the only way to get a personalised annuity rate based on your unique situation.

• Don’t settle for less – seek out the highest offer because small differences in annuity offers can add up to large amounts over a long retirement.

|