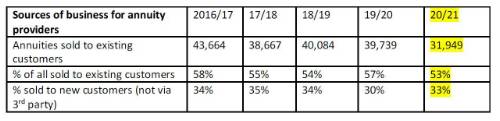

Latest figures from the Financial Conduct Authority suggest misplaced loyalty and inertia may be eclipsing extra cash, with 53% of GIfL plans purchased in 2020/21 sold by pension companies to their existing customers.

“The new rules won’t work unless providers help their customers to secure the extra income,” said Stephen Lowe, group communications director at retirement specialist Just Group. “Providers who do the minimum are more likely to keep the customer’s business and the FCA’s figures show the numbers switching has barely improved.

“Industry quotes show that a 65-year-old in reasonable health with an average GIfL purchase (£68,000) would miss out on £490 a year extra income by accepting the lowest offer (£3,324 a year) compared to the best (£3,814 a year), equal to £12,250 over 25 years. However, health history and lifestyle information could push that much higher.

“Since 2019 your existing pension provider has been obliged to show you how its own Guaranteed Income for Life quote compares with the best on the market. The idea being that seeing the difference will encourage people to switch but the FCA’s figures show this doesn’t seem to be happening,” said Stephen Lowe.

“Customer decisions are heavily influenced by the level of support they are offered. Forward-thinking providers are actively helping their customers by providing modern broking services that make it easy for their customers to compare and switch.

“Many providers are still dragging their feet, knowing if their customers don’t get that level of support, they are more likely to stay put and accept less competitive offers.”

FCA Retirement Income Market figures show that more than half (53%) of the GIfLs sold are by providers to their own clients:

“The message for customers is to check if your provider offers a broking service to help you get that better rate. If they don’t then take a moment to consider how much that extra income will add up to over 20 or 30 years of retirement, then decide whether you want to take the first deal on offer.”

He said people using a pension fund to buy a Guaranteed Income for Life product should:

• Understand your own provider may well not offer you the best deal on the market.

• Take up their entitlement to a free appointment with the independent and impartial guidance service Pension Wise to help understand how to make the most of their pension.

• Where providers do not offer a broking service, consider using an independent service or a regulated financial adviser who will work on your behalf to find the most suitable solution for your circumstances and compare costs with the fees your provider would charge.

• Ensure that medical and lifestyle information is taken into account so that the income offered reflects their unique personal circumstances.

|