|

|

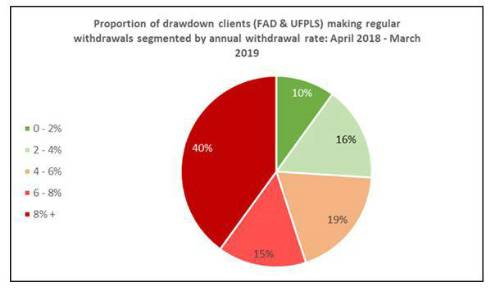

Alarm bells should be ringing following the publication of withdrawal rates from pensions, according to Stephen Lowe, group communications director at Just Group. Following today’s publication of the Financial Conduct Authority’s latest Retirement Income Market data bulletin for 2018-19, he said: |

“Once again the data raises concerns with more than half (54%) of all pensions accessed last year completely emptied out. More than 350,000 pensions were fully withdrawn with an average size of nearly £13,000 so these are by no means insignificant pensions. “Even where pension money is left invested and regular sums taken, the withdrawal rates are far higher than most experts would consider sustainable for a long-term investment such as a pension. “The FCA figures show that four in 10 (40%) drawdown customers took more than 8% of the fund value a year although for those with funds of less than £50k this rises to nearly two-thirds (63%). Overall 74% of people are taking more than 4% of the fund value each year. “This contrasts with guidance from organisations such as the Institute of Faculty of Actuaries suggesting 3.5% would be more a more suitable drawdown rate for a 65-year-old and 3% for a 55-year-old. “Many of the long-standing problems with the retirement market appear to be alive and well despite the apparent panacea of the pension ‘freedom and choice’ reforms. For example, most drawdown plans sold are to the providers’ existing customers.

“The number of annuity buyers achieving enhanced rates is also disappointing at less than four in every 10. We welcome the additional changes the FCA is bringing to this area to try to highlight the best rates in the market to those consumers seeking the security of a guaranteed income for life.” |

|

|

|

| Take the lead client-facing projects ... | ||

| Various locations - Negotiable | ||

| Choose Life! Choose a major global co... | ||

| Various locations - Negotiable | ||

| Actuarial skillset? Apply now for Snr... | ||

| South East / hybrid with travel requirements - Negotiable | ||

| Financial Risk Leader - ALM Oversight | ||

| Flex / hybrid - Negotiable | ||

| Be the very model of a modern Capital... | ||

| London - Negotiable | ||

| Pensions Actuary seeking a high-impac... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Great opportunity for Pensions Actuar... | ||

| London or Scotland / hybrid 3dpw office-based - Negotiable | ||

| Responsible Investing Manager - Clima... | ||

| London/Hybrid - Negotiable | ||

| Quant Strategist | ||

| London/Hybrid - Negotiable | ||

| Multiple remote longevity contracts | ||

| Fully remote - Negotiable | ||

| Multiple remote inflation hedging con... | ||

| Fully remote - Negotiable | ||

| Play a vital role in shaping a new He... | ||

| London or Scotland / hybrid 50/50 - Negotiable | ||

| Support the Longevity team of a globa... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

| Delve into financial risk within a ma... | ||

| Wales / South West / hybrid 1dpw office-based - Negotiable | ||

| Project-based Life Pricing Actuarial ... | ||

| South West / hybrid 2 dpw office-based - Negotiable | ||

| Pricing Actuary | ||

| London - £120,000 Per Annum | ||

| Develop your career in motor pricing | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Experience real career growth in home... | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Be at the cutting edge of technical p... | ||

| UK-wide / hybrid 2 dpm office-based - Negotiable | ||

| Use your passion for innovation and t... | ||

| London / hybrid 2 days p/w office-based - Negotiable | ||

Be the first to contribute to our definitive actuarial reference forum. Built by actuaries for actuaries.

Copyright © 2026 Actuarial Post. Created by Zero-One Design Ltd