Tyron Potts FIA,Associate - Head of Pensions Research, Barnett Waddingham

Most occupational pension schemes pay a surviving spouse a percentage of the member’s benefit after the member dies. However, under the terms of the 2010 Equality Act, schemes could exclude civil partners and same-sex spouses from entitlement to survivors’ benefits, to the extent that the pension was accrued by the member before 5 December 2005 (when civil partnerships became legal in the UK).

This exemption has now been ruled as incompatible with EU law by the Supreme Court.

During the hearing, the government noted that the cost of applying the ruling retrospectively would be £100m in total for private sector pension schemes and a further £20m for public sector pension schemes.

Not all schemes will be affected in the same way, and a key point in determining the impact will be whether the scheme made use of the exemption in the 2010 Equality Act. Trustees of schemes in this situation should discuss the position with their legal advisors. It may be necessary for the scheme rules to be changed, and any restricted benefits will need to be recalculated (and back payments may need to be made).

Longer-term, there may also be costs to schemes and sponsors depending on the benefits provided and the number of scheme members in same-sex marriages. Currently only around 2% of marriages* are between same-sex partners, so for many schemes it is unlikely that substantial adjustments will be required.

*ONS 2014 data

Principle of “no retroactivity”

The outcome of this case appears to hinge on when the entitlement to a spouse’s pension arises. The lead judge held that the survivor’s pension liability arose at the time of the member’s death, rather than while the main benefits were accrued, or at the date of retirement for example. Therefore, the widow’s benefit should be paid on an equal basis as for heterosexual marriages. The lead judge was happy that this decision did not represent a retroactive application of the law.

Interestingly, the judges in the Walker v Innospec case explicitly considered the Barber judgement, the effects of which were limited to pension benefits accrued after 15 May 1990. However, they agreed the Barber limitation to be exceptional and therefore, we should not expect a re-opening of that particular can of worms!

Trustees and sponsors could use this ruling as a prompt to review the assumed proportion of married members used in assessing the scheme’s funding position.

Many schemes adopt similar, relatively prudent assumptions for the likelihood of dependants’ benefits being due, which have not been varied for a number of years. They typically assume a fairly high proportion of scheme members are married at retirement (often around 80-90%) and this figure will remain constant over time.

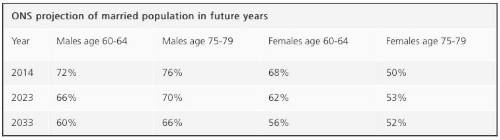

In fact the percentage of people in the UK who are married or co-habiting has generally declined in recent years, and this rate is expected to continue to decline according to projections from the Office for National Statistics. The ONS projects that, by 2033, there will be a fall of around 10% in the proportions of people married in their 60s and 70s, compared to 2014:

A review of the proportion married assumption does not necessarily lead to an increase in the expected cost of funding the scheme, and in fact could potentially reduce the funding cost. For employers, a review of proportion married assumptions could also potentially reduce liabilities on an accounting basis, although again the effects are not likely to be especially material.

Nevertheless, in cases where the scheme has to increase (and/or backdate) spouse’s pensions already in payment, then there will be a funding cost which, for a small scheme in particular, might be significant.

Trustees should take care for example if benefits have been secured via a ‘buy-in’ policy. Wording should be reviewed to ensure that this ruling doesn’t then lead to a mismatch of benefits insured against those actually payable from the scheme.

Ji-Hyang Lee contributed to the writing of this

|