Ian Mills BSc FIA, Senior Investment Consultant, Barnett Waddingham

“But sometimes risk can appear in unexpected places and the best solution can be the opposite of what you expect. In this case we had to go beyond the expected to get the best result.”

We all know that investing in overseas assets gives us currency risks. This is intuitively obvious. If I buy shares in a Hong Kong bank, or a Kazakhstani mining company, and the exchange rate subsequently moves, then my investment’s value in pound terms will have changed. When the pound “weakens” then the pound-value of my overseas investment will go up, or vice versa.

Given the current Brexit uncertainty, this is a hot topic right now. Every time there’s big news that affects the most likely Brexit outcome, then the value of the pound versus the dollar, or the euro, moves significantly. When a hard Brexit looks more likely, the pound tends to weaken, and vice versa. So because no-one knows how Brexit is going to play out (if at all!), we’ve been talking with a lot of our clients about currency hedging strategies. I’m sure many other investment consultants have too.

When a hard Brexit looks more likely, the pound tends to weaken, and vice versa.

So many investors looking overseas will put in place currency hedging strategies to protect them from the vagaries of the currency markets. The largest institutional investors, like the biggest pension schemes or big insurance companies, might do this directly by using derivatives. Smaller investors can still hedge currency risks, as many off-the-shelf pooled funds come in both currency-hedged and currency-unhedged flavours. But what is easily missed is that domestic investments can come with currency risks as well. In fact, around 70% of the income of FTSE 100 companies comes from outside the UK, and so UK equity investments are therefore exposed to currency risk too. We call this indirect currency risk.

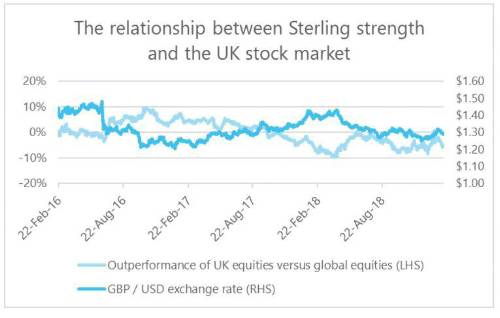

This isn’t just theoretical, our analysis shows that because there’s so much overseas income the FTSE 100 is now negatively correlated to the strength of sterling. This chart shows the GBP/USD exchange rate compared to the relative performance of UK equities versus global equities. It’s clear from the chart that, recently at least, when the pound goes down the stock market tends to go up, and vice versa.

For the statisticians, the correlation between the UK market’s relative performance and the GBP/USD exchange rate has averaged around -80% since February 2016, when the Brexit vote was announced in Parliament. This is the opposite of what I was taught to expect as a young trainee investment consultant – I was taught that things that are bad for the pound are also bad for the UK equity market. They were expected to be positively correlated.

The biggest investors can put in place currency derivatives to manage this risk. However, for smaller investors (like most pension schemes) there’s no way to manage it. There simply aren’t pooled funds out there that put in place currency hedges over UK equity portfolios.

“So, this leads to a counterintuitive conclusion. To reduce currency risk you might need to invest less domestically and more overseas!”

In fact, this is exactly what our client has done – they’ve switched assets overseas because it makes the currency risk easier to hedge. There were other reasons too, but in effect, they’re switching from assets with indirect but unhedgeable currency risk into assets with direct but hedgeable currency risks. They were able to keep their overall equity allocation constant, but because their overseas equity pooled fund comes in both currency-hedged and currency-unhedged flavours, they can now manage the currency risk better.

Of course, there are other issues to consider too. Whilst investing more overseas was the right thing to do for this investor, what’s right for you could be very different. It will depend on your portfolio, your objectives, and your constraints. The important thing is to get good advice that considers all the options – not just the obvious ones.

|