By Andreas Schraft, Head Cat Perils, Swiss Re. By Andreas Schraft, Head Cat Perils, Swiss Re.

In 2011, USD 370 billion was lost to the global economy through natural catastrophes. Insurers and reinsurers were able to cover around USD 116 billion, but this leftUSD 250 billion in uninsured losses to be paid by affected companies, private households, governments, development agencies, NGO's, or charity organizations.

Insurers are willing and able to close the gapon catastrophe losses. Improvements have been made in understandingthe insurability of large-scale natural disasters. The industry is also getting better at bringing risk management principles to governments and private sector partners, enabling a more holistic approach to disaster management where cost-effective prevention measures can be put in place to curb the impact of natural disasters and lessen the burden on post-disaster financing.

Of all the natural catastrophes,perhaps floodingbest illustrates the issues influencing insurability and catastrophes. Floods affect more people than any other natural catastrophe. Recent events have proven that floods can rival major earthquakes or hurricanes in terms of economic and insured losses. Climate change, population growth and higher concentrations of increasingly vulnerable assets will almost certainly lead to higher losses from floods.

The first problem facing insurers is defining a flood event. The common denominator is water and the damage it causes. However, the range of natural events which can bring about a flood are varied: torrential rainfall, flash flooding, river floods, storm surge, tsunami, dam burst, ice jam, mudflow, volcanic melting of ice caps and rising groundwater can all lead to flooding, and this list is by no means exhaustive. These varied sources of "flood" are extremely relevant for insurers because they significantly different risk patterns. In some cases, it may be difficult to differentiate a flood loss from another peril, as was illustrated by Hurricane Katrina in 2005.

Insurance works when risk is shared among a critical mass of policyholders. For flooding, the most significant obstacle to insurability is building a sufficiently large and varied number of participants.The problem is thatthose living in highly exposed areas tend to seek more coverage than those less at risk.If the risk is not adequately shared throughout the population, the economic viability of insuring against flood may be challenged. Insurers may either have to charge unaffordable premiums, or simply not offer insurance.

Another key principle is assessability. State-of-the art models, field inspections and a good measure of common sense have made floods more assessable. Statistics alone, however, are not entirely reliable since catastrophic flood losses have such a low probability of occurring. Further, the risk landscape is dynamic. Urban growth means that safe areas can still be inundated if natural drainage areas are built over. The situation may further be complicated when an insured areais part of a complex manufacturing chain and business interruption losses occurin entirely different parts of the world.

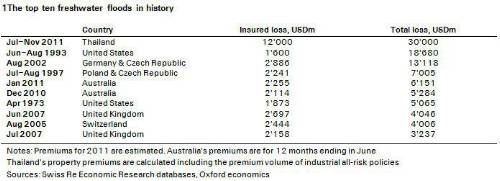

At USD 12 billion, Thailand's 2011 flooding was around USD 10 billion more expensive in both insured and economic losses than any other flood event on record. Thehigh cost was attributable to many factors; however, one highly significant issue arising from this floodis the presence of a so-called"hot spots". In Thailand, a large cluster of highly flood-vulnerable electronics, car manufacturing and clothing industries was concentrated along a flood-prone river. These industries were significant to the global manufacturing supply-chainand losses were not just incurred in the flooded region, but globally. In fact, 70% of insured losses for this event were written outside Thailand.

The challenge for the insurance industry is to develop the necessary tools to identify similar hot spots elsewhere. Swiss Re has developed an approach to identifying flood hot spots. High resolution flood data can be overlaid on countries or regions with similar economic characteristicsto Thailand. By examiningcompany data on foreign-controlled subsidiaries, regions can be identified which have a high level of business conducted by foreign parent companies. This is one indicator of a high share of international insurers in these risks, which in turn makes the monitoring of accumulations more challenging. In addition, the insurance conditions present in these regions and surveys with local risk experts can be used.

In the initial study, China tops the hot spots rankingfollowed by the remaining BRICs. Poland and Vietnam have also shown up as countries requiring closer observation.

Traditionally, the insurer's role takes place in post-disaster financing. Recent years, however, have seen agreater emphasis on utilising insurance expertise to advise decision-makers on cost-effective measures to prevent losses. Such measures can be quite practical: such as building flood walls or rehabilitating coastal sand dunes. They can also take place at the regulatory level, where governments are encouraged to put adequate building or zoning regulations into force or where compulsory insurance is put in place to ensure a broad insurance population.

The scale of catastrophe losses in recent years has emphasised the importance of public-private partnerships in catastrophe risk management. 2010 and 2011 have both shown the necessity of closing the insurance gap and reducing the costs to society from natural disasters.

|