But new research from Royal London – ‘Will Housing Wealth Solve the Pensions Crisis?’ - shows that for most retirees, housing wealth is unlikely to be a ‘get out of jail free’ card to deal with inadequate pension savings. It concludes that the challenge of 12 million people not saving enough for their retirement will not be solved by assuming that those who fall short on pensions can simply live off the value of their home.

The research uses data from the Wealth and Assets Survey to look at the pension income and housing wealth of nearly 7,000 pensioners across Great Britain. In particular, it examines how far those with poor pensions are sitting on significant amounts of housing equity. The key findings are:

Whilst those with the highest pensions are almost all home owners, around a third of the poorest pensioners are still renting in retirement and have no housing equity to draw on;

The people with the most housing equity tend to be the same people who have the highest pensions; amongst the poorest fifth of pensioners, the average housing equity is only around £150,000, compared with just over £400,000 for the richest fifth;

The main exception to this rule - that is lower income pensioners who may have a worthwhile amount of housing equity - are those in London and the South East, particularly those who benefited from the ‘right to buy’ their council house back in the 1980s and 1990s; some divorced pensioners and some widows as well as those with inherited wealth may also be exceptional in combining modest pensions with meaningful amounts of housing equity;

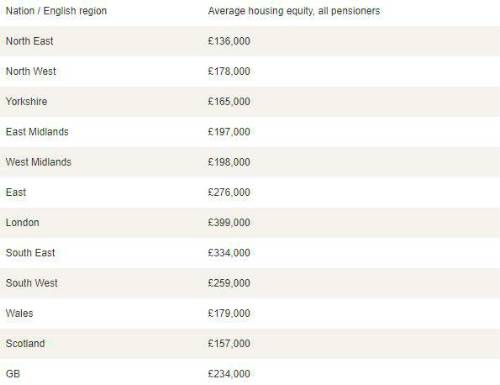

Average housing equity levels amongst retired pensioners as a whole vary from just £136,000 in the North East of England to £399,000 in London, as show in the table:

Source: Royal London calculations based on Wealth and Assets Survey, Wave 5 (2014-16)

Even for those with housing equity, equity release providers will often only allow a pensioner to borrow only around a third of the value of their property if they take out the policy at retirement; most policies come with a ‘no negative equity guarantee’, and because of the impact of compound interest on equity release loans through retirement, lenders want to make sure that the borrower retains significant equity at the start of the policy;

Releasing housing equity through ‘downsizing’ is likely to be unattractive for most; the supply of ‘step down’ retirement accommodation is limited and often expensive, reducing the amount that can be freed up by downsizers; newly retired families are also often reluctant to sell up and move away from networks of families and friends, and may not want to eat into housing equity that they plan to pass on to their children;

Even though home ownership rates amongst retirees are currently at record levels, this is unlikely to be sustained; even among 45-64 year-olds, home ownership rates are starting to fall, and the declines are even greater for younger households;

Commenting on the findings, Steve Webb, Director of Policy at Royal London said: “Official figures suggest that around 12 million people of working age are not saving enough for their retirement. It might be tempting to think that as long as such people are homeowners in retirement then they can top up meagre pensions by using the value of their home. But this research shows that even owning a home is not a ‘get out of jail free card’ for those with poor pensions. Many of those with low pensions also have relatively small amounts of housing equity, and lenders will often lend only a small percentage of the value of your home. Whilst using housing equity will help some groups of poorer pensioners, particularly in London and the South East, for most there is no substitute to building up a decent pension for a comfortable retirement”.

|