Steven Cameron, Pensions Director at Aegon, sets out what that might mean in practice: “At present, individuals who contribute to pensions receive tax relief linked to the rate of income tax they pay *. If you are a basic rate taxpayer you receive tax relief at 20% which means £100 from your take home ‘after tax’ pay into a defined contribution pension is boosted to £125 after £25 bonus from the Government. Higher rate taxpayers receive 40% tax relief and additional rate taxpayers earning over £150,000 get 45% relief**.Contributions from employers boost these amounts further.

“The Chancellor is rumoured to be considering changing the system so that rather than pensions tax relief varying with your income tax rate, everyone would receive a flat rate relief of 25%. This is seen by many as a fairer way of sharing this Government incentive across people of all earnings bands but would also likely produce a cost saving for the Treasury. It would be good news for basic rate taxpayers who’d receive a more generous bonus but would create a big dent in the future pension pots of higher and additional rate taxpayers unless they increased their contributions.

“Under a flat rate of 25% tax relief, a basic rate taxpayer paying £100 a month into their defined contribution pension would see this topped up to £133.33 rather than the current £125, an extra £8.33. However, a higher rate taxpayer who currently sees their £100 increased to £166.66 would see this reduced to £133.33.

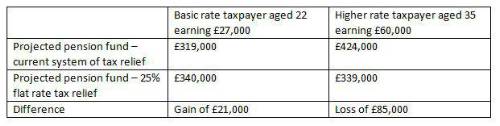

“A basic rate taxpayer on average earnings of £27,000 paying 4% out of take home pay from age 22 through to their state pension age (68) could see the fund from their contributions increase from £319,000 to £340,000. But a higher rate taxpayer aged 35 earning £60,000 paying the same 4% from take home pay would see the fund from their contributions fall from £424,000 to £339,000 – a fall of £85,000. To maintain their retirement aspirations, this higher rate taxpayer would need to increase their contribution out of take home pay to 5% or in this example by £50 per month initially.

Winners and losers from a 25% flat rate of pensions tax relief

This table gives examples of how much 2 individuals might have in their pension fund by their state pension age (68) under the current tax relief rules and under a flat 25% tax relief. Both assume personal contributions of 4% of total earnings

“As well as tax incentives on contributions, individuals can take one quarter of their pension proceeds tax free, with the balance being taxed as income at the rate they pay in retirement. This means pensions are already regarded as the most tax efficient means of saving for retirement and the rumoured changes would make pensions an even better deal for those paying basic rate income tax.

“Most individuals paying higher rate tax when working pay basic rate income tax once they’ve retired. For them, pensions would still be very tax efficient under a flat rate 25% tax relief system. The group for whom it’s less clear are those who might be higher rate taxpayers in retirement, who might need to weigh up the pros and cons. But like all employees who contribute to a workplace pension, they would also receive valuable employer contributions offering an additional attraction.

“Before implementing a move to a flat rate of pensions tax relief, more thinking is needed on how this would work for those contributing to a defined benefit or final salary scheme. Here, the pension benefits they receive are based on their final or career average salary and not on the amount their contributions grow to after tax relief and investment growth. For consistency with those contributing to defined contribution schemes, higher and additional rate taxpayers in defined benefit schemes might see their and their employer’s contributions taxed as a benefit in kind, increasing their tax bills.”

How contributions would be increased after the Government tax relief

|