The number of women preparing adequately for retirement is at an all-time low and remains well behind the preparation levels of their male counterparts, according to the Scottish Widows 2013 Women and Pensions Report.

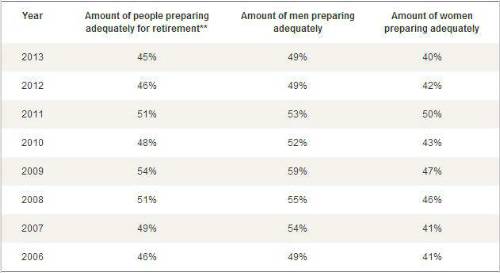

Just 40% of women, compared to 49% of men, are preparing adequately for later life, a drop from 42% last year and 50% in 2011.

The ninth annual survey of over 5,000 people found that while over a third (37%) of women have no pension whatsoever, the same applies for just over a quarter (27%) of men. The picture is little better for those women who are saving, with the report finding that they are only managing to put aside £182 a month on average, well below the average amount of £260 amongst men. This creates a gender pension savings gap of nearly £1,000 a year.

Amount of people preparing adequately for retirement, by gender:

**Saving adequately refers to those saving at least 12% of their income or expecting their main retirement income to come from a defined benefits pension

Lynn Graves, Head of Business Development, Corporate Pensions at Scottish Widows, commented: "It is worrying to see that women are continuing to lag behind men in retirement savings. The number of women preparing adequately for retirement has dropped from last year to a record low. This growing gender gap in retirement savings means that women are facing an ever increasing shortfall when it comes to retiring and must act now to ensure they will not be left exposed in later life."

Generational barriers to saving

The report found that women are coming up against barriers to saving at every stage of life, with different lifestyle factors taking their toll on women of different ages.

Women in their 20s were found to be tied down by short-term financial pressures and are prioritising living expenses (42%), paying off debts (26%), travel and holidays (23%), or saving for a property (18%) over saving for retirement. Over half (54%) of 22-29 year olds don't have a pension, compared to 37% of the general female population.

Perhaps due to family commitments, only 50% of women in their 30s work full-time compared with 81% of men of the same age, meaning 30-something women bring in an average gross income of £19,200 - way behind the £28,700 that the average 30-something man takes home. Career breaks and cutting back on hours have a knock-on effect on women's ability to save, with women in their 30s only saving £87 a month on average towards retirement, outside of pension and property investments. This is compared with the £151 that their male counterparts are saving each month outside of pensions and property.

By the time women reach their 40s, their financial priorities have changed, with almost 1 in 4 (23%) 40-49 year olds saying they had prioritised financially supporting their children over retirement saving in the last five years. 24% also said they expect their partner's income to help support them in retirement, despite the fact that 79% do not know what their partner would be entitled to from their pension fund if they were to separate.

Despite their proximity to retirement age, paying off debt is still at the forefront of the minds of women in their 50s, with 1 in 4 (24%) women of this age still considering paying off debt a bigger priority than saving for retirement. Women in their 50s still owe an average amount of £11,400, slightly higher than the £11,000 of average debt women in their 40s have.

Lynn Graves continued: "We have identified the different barriers preventing women from saving at every life stage, helping us to see where this gender savings gap is coming from and understand how best we can support women to help them overcome these barriers.

"Of particular concern is the number of women in their 40s who are planning to rely on their partner to help support them in retirement, but are unsure of what their pension provision would be were they to separate. We should encourage these individuals to take full responsibility for their financial independence. Knowing what you are entitled to allows you to make informed choices and gives you a back-up plan if anything were to go wrong.

"The pensions industry, Government and employers need to work together to raise awareness of the unique lifestyle pressures that take their toll on women's savings at different ages and help women prioritise their pensions. Initiatives such as auto-enrolment are fundamental in helping the nation's workers to think about saving, but women outside the workplace need greater access to information and guidance about other retirement options."

|