By Kim Durniat FIA, Partner and Head of Life Consulting at barnett Waddingham

In this article we will discuss different approaches firms may take to reflect the uncertainty with the valuation, including holding additional reserves and the importance of performing sensitivities.

How can insurers set the right reserves?

Although it has been over a year since the outbreak of the virus, there remain a lot of uncertainties. These include the impact on recovered individuals’ long-term health, the timing of vaccine rollout and how long the recession will last.

At the start of the pandemic, insurers were hesitant to hold extra reserves in relation to the pandemic. This makes sense as there was little or no data to help firms to set these reserves.

However, now that we have almost a full year of data, we are seeing an increasing number of firms looking to hold additional “short-term” reserves for the impact of Covid-19 and reassessing their experience at year-end with the nine to twelve months of pandemic data that they have available.

At present, a short-term reserve seems a sensible option compared to ignoring the virus or incorporating the abnormal experience in long-term assumptions.

To do this, it is clear that experience monitoring has a vital part to play. Firms should look at their 2020 experience in detail to understand the impacts of Covid-19 on claims to date. They also need to consider the likely impacts of the third wave of the pandemic in the first quarter of 2021.

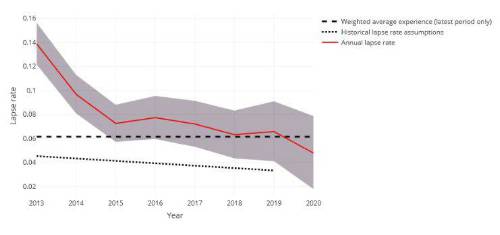

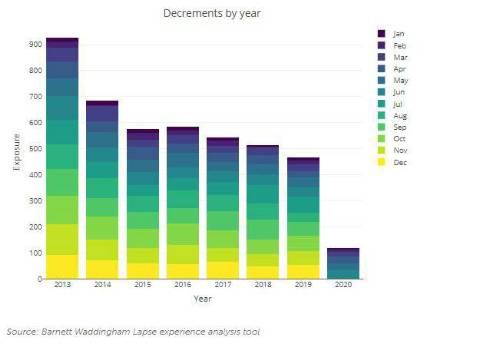

Here at Barnett Waddingham we are helping clients monitor experience in “close to real time”, with a detailed breakdown to understand where experience has differed by month, sales channel and even UK region as the virus developed throughout 2020.

Below are two snapshots from one of Barnett Waddingham’s experience monitoring tools.

We believe it is through this level of analysis that firms can confidently challenge the need for a short-term “Covid-19” reserve and have the evidence to back up this number when presenting to the Board.

Given the ongoing uncertainty about the impacts of the virus, any historical analysis will need to be supplemented by expert judgement. However, the historical analysis is a vital ingredient. Without this it will be impossible to confidently argue for or against the need for any additional reserves, or to justify the level of any additional reserve proposed.

Providing context through sensitivities

Regardless of whether or not you establish an additional reserve for Covid-19 related claims, the Board needs to understand the potential impact of the pandemic on the firm, from both insurance and wider economic risks.

A good valuation report should be to help the Board understand the solvency position of the business and highlight the risks and uncertainty around this position. Only with this information can the Board make better informed decisions. With all the additional uncertainties around Covid-19, performing sensitivities and stress and scenario testing / analysis is more important this year-end than ever.

While many insurers may undertake the bulk of stress and scenario testing when carrying out their own risk and solvency assessment (ORSA), it is important to ensure that sufficient analysis is conducted as part of the year-end valuation. For some, this may mean accelerating some of the work typically performed as part of the ORSA process. It is imperative that the Board understands the resilience of the balance sheet and the degree of adverse experience the firm is able to withstand.

Avoiding a ‘tick-box’ exercise

Firms may have a list of sensitivities that are performed year on year, do not change and are not challenged. This is inappropriate. It is crucial to avoid sensitivities being seen as a ‘tick box’ exercise.

All firms must continuously challenge the sensitivities performed and adapt them as the business and external influences change. In our opinion it would be rare for there to be no required changes year-on-year.

A critical review of scenario analysis is especially important for year-end 2020. Firms may have made significant changes to their risk management framework, dividend policies or the way risks are managed. Any changes will need to be considered when performing stress and scenario testing to ensure all potential risks are being captured.

|